Introduction

AI investment in financial services is accelerating - yet most institutions running pilots cannot point to measurable enterprise-scale returns. According to research from Lorikeet CX, 59% of financial services leaders report using AI, but most struggle to quantify the ROI.

The gap isn't the technology. It's readiness.

Institutions that stall at the pilot stage typically share the same profile: fragmented data, governance frameworks bolted on after deployment, and executives who can articulate AI's potential but not its operational requirements. This guide is built around that profile.

What follows is a practical framework for assessing AI readiness across five dimensions - strategy, data, governance, talent, and infrastructure - with specific attention to the constraints that make financial services different from every other industry.

Key Takeaways

- 59% of financial services leaders use AI, but measurable enterprise-scale ROI remains elusive for most

- Highest-value use cases right now: fraud detection, AML/KYC compliance, and internal productivity tools

- AI readiness requires five pillars: strategic alignment, data quality, governance, talent, and infrastructure

- Governance embedded from day one determines whether deployments scale or stall

Where Financial Services Firms Actually Stand on AI Today

Most financial institutions are using AI. Few have scaled it.

The contrast is stark: widespread experimentation sits alongside limited production deployment. The "pilot trap" is real - institutions run proofs of concept, see promising results, then discover they lack the data infrastructure, governance maturity, or organizational alignment to push beyond controlled environments.

The Large vs. Small Institution Divide

Large banks have been investing in AI infrastructure for years - building proprietary models, hiring data science teams, and acquiring AI capabilities. Smaller institutions are now closing the gap faster than expected, using SaaS platforms and low-code tools that don't require the same capital investment.

This shift matters because it changes the competitive dynamic. Community banks and credit unions that previously couldn't afford enterprise AI now have access to these same capabilities - but face the same readiness challenges as their larger counterparts, often with fewer internal resources to address them.

The Agentic AI Horizon

Closing that readiness gap matters more now because the next phase of AI is already arriving. Generative AI drove most recent adoption growth through internal productivity applications - but the shift toward agentic AI changes the stakes considerably. Agentic systems don't just respond to prompts; they act with a degree of autonomy, executing multi-step workflows and making decisions within defined parameters.

A survey by MIT Technology Review on agentic AI in banking found that trust and governance rank as the primary barriers to autonomous AI adoption in financial operations - above cost or technical capability. Institutions that build governance infrastructure now will be positioned to deploy agentic systems when they're ready. Those that wait will hit those same barriers under competitive pressure, with less time to address them.

The High-Value Use Cases Gaining Traction in Financial Services

Enterprise-wide AI deployment remains rare. Most ROI is being generated in specific, bounded use cases with clear success criteria and meaningful human oversight. Four categories stand out.

Fraud Detection and AML/KYC Compliance

Fraud detection is the most widely deployed AI use case in financial services, and the reasons are straightforward. These workflows are rules-heavy, high-volume, and involve pattern recognition at a scale that humans simply cannot match. AI excels at detecting anomalies - including novel fraud patterns tied to cryptocurrency transactions and cross-border financial crime - that traditional rule-based systems miss entirely.

One critical governance consideration: AI models flagging transactions still require explainable outputs for regulatory reporting. Under frameworks like SR 11-7 and CFPB adverse action guidance, institutions must be able to explain why a transaction was flagged or a credit decision was made.

That makes transparency a technical requirement embedded in the model architecture - not a compliance checkbox added after deployment.

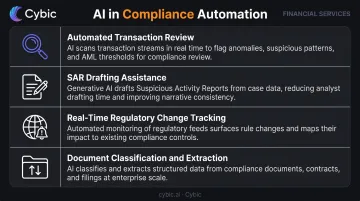

Compliance Reporting and Regulatory Automation

Compliance is an ideal entry point for AI adoption - internal, rules-based, and extremely high in volume. Financial institutions file hundreds of thousands of Suspicious Activity Reports annually, each requiring structured analysis and narrative drafting that consumes significant compliance team time.

AI is reducing this burden through:

- Automated transaction review and pattern flagging

- SAR drafting assistance that produces structured first drafts for human review

- Real-time regulatory change tracking across jurisdictions

- Document classification and extraction for regulatory filings

Because these workflows are internal and rule-bound, the governance risk is lower than customer-facing AI - making compliance automation a practical first deployment for institutions proving out their AI capabilities before expanding scope.

Operational Efficiency and Internal Productivity

Internal productivity tools are generating some of the fastest returns with the lowest governance risk. The highest-adoption use cases include:

- Knowledge management search - AI-powered retrieval tools that help analysts surface institutional knowledge, research, and policy documents faster

- Legacy code modernization - AI-assisted tools for documenting, translating, and modernizing COBOL systems, which still underpin a large share of banking transaction processing

- Intelligent document processing - AI and OCR-based systems that extract, classify, and route structured data from loan applications, KYC documents, and regulatory filings

Cybic's Intelligent Document Processing capability supports exactly this kind of work - extracting, classifying, and routing documents across financial services workflows that have traditionally required large manual teams to manage.

Customer Experience and Personalization

Customer-facing AI carries a different risk profile than internal automation. Nondeterministic outputs from generative AI models create real regulatory exposure when they reach customers directly.

Common use cases in this space include:

- Conversational chatbots for account inquiries and support

- Recommendation engines for product cross-sell and financial planning

- Proactive financial coaching and spend alerts

Most large banks are keeping these capabilities internal or in limited pilots. Digital-first institutions and smaller players are moving faster, but the ones seeing durable results build in human-in-the-loop review for any AI output that reaches customers directly.

The Five Pillars of AI Readiness for Financial Institutions

AI readiness is not binary. An institution can have excellent data infrastructure and weak governance, or strong executive alignment and no AI talent pipeline. All five dimensions need honest assessment before meaningful deployment can happen.

Pillar 1: Strategic Alignment and Executive Fluency

AI initiatives without executive understanding of both the opportunities and the operational risks tend to produce fragmented, underfunded projects that stall before reaching production.

Executive alignment looks like:

- Cross-functional working sessions where business and technology leaders develop shared language

- Board-level recognition of AI as a strategic function - not a technology experiment

- Clear prioritization of use cases against business outcomes, not technology novelty

- Defined accountability for AI outcomes at the leadership level

Without this foundation, individual teams build isolated tools that never connect to institutional priorities - and data quality problems compound the damage.

Pillar 2: Data Foundation and Quality

AI systems are only as reliable as the data feeding them. Financial institutions face particularly acute data readiness challenges:

- Siloed systems - core banking, CRM, risk, and compliance platforms that don't share data in real time

- Untagged on-premise data - large volumes of institutional data that exist but aren't structured or accessible for AI use

- Inconsistent definitions - the same field (customer ID, transaction category, risk rating) defined differently across business units

- No single source of truth - multiple versions of the same data living in different systems with no reconciliation

Data cleanup is consistently the most time-consuming part of AI readiness. Data scientists report spending up to 80% of their time on data preparation rather than model development. Cybic's data strategy engagements begin with a data landscape audit and gap analysis because this foundation determines whether AI deployment succeeds or stalls.

Pillar 3: Governance and Risk Framework

Governance readiness means having model risk management protocols, auditability mechanisms, explainability standards, and escalation procedures in place before deployment - not assembled afterward when regulators ask.

Governance embedded into architecture from the start accelerates deployment. Retrofitting compliance onto a live system is slower, costlier, and riskier than building it in.

SR 11-7 model risk management guidance provides the foundational framework for US institutions, covering model development, validation, and ongoing monitoring.

Pillar 4: Talent and AI Literacy

The skill gap spans multiple dimensions simultaneously:

- Data science and ML engineering for model development

- AI ethics and fairness assessment

- Regulatory fluency to understand which governance requirements apply

- Change management to drive adoption across the organization

AI literacy for non-technical employees is as important as technical hiring. Adoption fails when front-line teams don't trust the tools, don't understand the outputs, or fear what AI means for their roles. Cybic's AI Adoption & Governance Frameworks service embeds change management alongside technical deployment for exactly this reason.

Pillar 5: Infrastructure and Technology Architecture

Infrastructure readiness requirements include:

- Ability to run AI workloads across cloud, hybrid, or on-premises environments without rebuilding every time the deployment context changes

- Integration pathways into legacy systems that don't require full system replacement

- Scalable data pipelines capable of handling real-time and batch AI workloads

- Role-based access controls ensuring the right people have access to the right systems and data

Cybic builds across AWS, Azure, and Google Cloud, with Snowflake and Databricks for data platform work. This means financial institutions can deploy where their data and compliance requirements dictate - and scale without rebuilding around a single vendor's ecosystem. Architecture decisions made now determine how quickly you can scale AI later.

Why AI Adoption Stalls: Key Barriers and How to Overcome Them

Understanding why pilots don't reach production is more valuable than optimism about AI's potential. Four barriers account for most failures.

Data fragmentation and quality Many institutions have only a fraction of their data genuinely AI-ready. The practical fix: build a unified data layer before selecting AI tools. Selecting tools first - then trying to retrofit them onto fragmented data - is what produces the integration failures that kill most deployments.

Regulatory uncertainty and compliance risk AI-specific regulation is still developing across transparency, bias, and explainability requirements. Rather than waiting for final rules, institutions moving forward successfully are adopting a principles-based governance approach. They build for explainability and auditability now - because incoming regulation will reward that foundation, not punish it.

Change management and AI literacy gaps The human side of AI adoption consistently proves harder than the technical side. Employees distrust tools they don't understand. Resistance emerges when AI is positioned as a replacement rather than a capability. Institutions getting this right lead with change management first and treat the technology as the implementation layer, not the headline.

Governance immaturity and explainability gaps More than half of financial institutions cite transparency and explainability as top barriers. This problem compounds as AI systems move from simple ML models toward complex agentic workflows. Vendor-supplied AI introduces additional risk:

- Institutions often lack visibility into how external models produce outputs

- Black-box outputs create real auditability exposure during regulatory review

- Without traceability, remediating model decisions after the fact becomes difficult

The further AI moves from interpretable models, the harder these gaps are to close retroactively.

Building AI Governance Into the Architecture - Not As an Afterthought

Governance bolted onto a deployed AI system creates compliance gaps, audit failures, and operational risk. By the time regulators or auditors ask questions, the system is already in production and patching it is expensive and disruptive.

Governance embedded at the architectural level works differently. It makes AI systems inherently safer, easier to audit, and faster to scale in regulated environments.

What Architecture-Level Governance Includes

In practice, this means:

- Role-based access controls (RBAC) - permissions tied to roles and responsibilities, not individuals, with systematic enforcement

- Encrypted data protection - in transit and at rest, across all environments

- Auditability and traceability - every AI-driven decision and workflow action is logged and traceable, so regulators, auditors, and compliance teams can verify behavior at any point

- Proprietary data protection - strict governance preventing client data from being used to train external or shared AI models

Cybic's Drava platform - their enterprise Data Intelligence to Automation platform - deploys these controls as structural features of the architecture rather than manual processes layered on top. Security controls, audit trails, and access restrictions are defined at the design stage, before a single workflow goes live.

Financial institutions that embed governance from day one can show regulators exactly how their AI systems operate, what decisions they made, and why. Institutions that don't confront that audit reckoning after deployment - when rebuilding compliance into a live system is both costly and operationally disruptive.

Frequently Asked Questions

What is the 30% rule in AI?

The "30% rule" refers to the principle that roughly 30% of an AI project's total effort should go toward data preparation and cleaning. In financial services, where data fragmentation and quality issues are pervasive, this figure often runs higher - making upfront data investment the single most important readiness factor.

What AI tools are available for financial services firms?

The main categories include:

- Fraud detection and AML platforms

- Compliance automation tools

- Internal knowledge management and search systems

- Developer assistance tools for legacy modernization

- Customer service AI

The right tools depend on the institution's specific use case priorities and governance requirements.

What does AI readiness mean for a financial institution?

AI readiness means the organization has strategic alignment, clean and accessible data, governance frameworks, capable talent, and the right infrastructure to deploy AI responsibly - and scale it over time. Running a pilot doesn't qualify; readiness is about sustained deployment capacity.

What is the biggest barrier to AI adoption in financial services?

Data fragmentation and governance immaturity are consistently cited as the top barriers. Most institutions have AI ambitions but lack the unified, accessible data and the auditability frameworks required to move beyond experimentation.

How do financial institutions govern AI while staying compliant?

Effective AI governance means embedding explainability, auditability, and access controls at the architecture level rather than applying them as compliance checklists after the fact. Aligning AI model risk management with existing frameworks like SR 11-7 model risk management guidance provides the foundational structure for US institutions.