Why 2026 Is the Defining Year for AI Governance in Financial Services

AI in financial services is no longer a pilot project or a proof of concept. It runs credit decisions, flags suspicious transactions, powers customer interactions, and drives AML workflows - often without the governance infrastructure needed to withstand regulatory scrutiny.

The gap between deployment speed and governance readiness is measurable. According to Grant Thornton's 2026 AI Impact Survey, only 18% of banking leaders were fully confident they could pass an independent review of their AI controls within 90 days - meaning 82% were not. The same research found that 50% of banks cite governance and compliance barriers as contributors to AI underperformance or failure.

That is not a readiness problem at the edges. It describes the majority of the sector.

This article addresses the three most pressing issues for financial institutions right now:

- The regulatory catalyst: the Financial Services AI Risk Management Framework (FS AI RMF), released in February 2026

- The four governance pillars institutions need to build

- How to move from policy documentation to operational controls that survive examiner scrutiny

Key Takeaways

- 82% of banking leaders lack full confidence in their AI controls - governance has not kept pace with deployment

- The FS AI RMF (February 2026) defines 230 control objectives spanning governance, data, model lifecycle, monitoring, third-party risk, and consumer protection

- Data governance, model lifecycle, identity and auditability, and third-party risk are the four pillars that matter most

- Governance failures are infrastructure failures - controls must be mapped to actual systems, not policy documents

- Agentic AI exposes accountability gaps that traditional model risk management was never built to handle

What the FS AI RMF Actually Requires

Origin and Authority

The CRI Financial Services AI Risk Management Framework was officially launched on February 12, 2026. It was developed through collaboration between the Cyber Risk Institute (CRI), the Financial Services Sector Coordinating Council (FSSCC), and more than 100 financial institutions globally. Treasury announced the framework on February 19, 2026 as part of the coordinated Artificial Intelligence Executive Oversight Group (AIEOG) deliverable series, positioning it within the President's AI Action Plan.

The FS AI RMF is structurally aligned with the NIST AI Risk Management Framework, adapted specifically for financial services conditions and regulatory expectations.

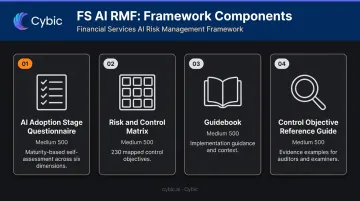

The Four Components

| Component | Purpose |

|---|---|

| AI Adoption Stage Questionnaire | Maturity-based self-assessment across six dimensions |

| Risk and Control Matrix | 230 mapped control objectives |

| Guidebook | Implementation guidance and context |

| Control Objective Reference Guide | Evidence examples that auditors and examiners will reference |

The 230 control objectives span governance, data management, model development and validation, monitoring, third-party risk, and consumer protection. These are not abstract principles. They describe system behaviors, ownership assignments, and evidence artifacts: the documentation expected to survive supervisory review.

The AI Lexicon

Released simultaneously, Treasury's AI Lexicon establishes common definitions across regulatory, technical, legal, and business functions. Terminology misalignment between engineering, risk, legal, and compliance teams is one of the most consistent reasons governance execution breaks down. Definitions drift between departments, controls get interpreted differently, and accountability becomes diffuse. The Lexicon creates a shared baseline that reduces that friction.

What Examiners Will Actually Ask

Regulators will use the FS AI RMF as examination scaffolding, similar to how FFIEC standards function for cybersecurity today. The questions examiners are likely to ask:

- Where is this control implemented in the system?

- Who owns it?

- What enforces it technically?

- What evidence demonstrates it is working?

- How is drift or degradation detected?

Narrative policy explanations will not satisfy these questions. System logs, access control records, test results, and monitoring dashboards will.

The Four Pillars of an AI Governance Framework for Financial Services

Pillar 1 - Data Governance

Data governance controls for AI go well beyond traditional data management. Requirements include:

- Data lineage tracking from source through training and deployment

- Training data documentation - provenance, versioning, sensitivity classification

- De-identification and privacy controls applied at intake, not post-deployment

- Feature store governance covering what inputs models consume

- Cross-border data flow management for institutions operating internationally

The sequencing matters. Sensitivity tagging must happen at data intake - retroactive compliance on training data is operationally difficult and legally exposed. Institutions relying on AI-driven underwriting or fraud detection could face regulatory consequences if models were trained on improperly sourced data.

Modular model architecture and lineage documentation are architectural safeguards, not documentation exercises.

Cybic's data governance practice includes metadata management and data lineage tracking as components of its data engineering engagements, reflecting this intake-first approach.

Pillar 2 - Model Lifecycle Governance

Model governance must cover the full development-to-retirement lifecycle:

- Documented development with bias testing built in

- Validation independence - the team validating a model should not be the team that built it

- Drift detection embedded in MLOps pipelines, not monitored manually

- Explainability thresholds calibrated to the risk level of the decision

- Automated re-identification regression testing before deployment

What "explainable" means depends entirely on the use case. A model used for consumer credit decisions requires more defensible documentation than one used for internal analytics. Institutions need to define that standard per use case and build it into documentation protocols - CFPB Circular 2022-03 makes clear that ECOA and Regulation B require specific, accurate adverse-action reasons even when complex algorithms are involved.

Pillar 3 - Identity, Access, and Auditability

The FS AI RMF places explicit requirements on how institutions manage both human and non-human identities interacting with AI systems. This pillar covers:

- Role-based access controls (RBAC) governing who and what can access AI components

- Decision-path auditability - logs that reconstruct what happened and why

- Cross-system logging for AI actions that span multiple platforms

- Immutable audit trails that can withstand examiner review

Governance platforms that embed RBAC, encrypted data protection, and auditability at the architectural level demonstrate what it means to build governance in rather than bolt it on.

Cybic's Drava platform takes this approach. Security controls, access governance, and traceability of AI-driven actions are built into the architecture from day one - not configured after deployment.

Pillar 4 - Third-Party and Vendor Risk

Institutions using third-party AI vendors or foundation models carry accountability for the outcomes those systems produce. Regulatory expectations under the FS AI RMF extend directly into vendor relationships, covering:

- Vendor transparency and documentation exchange

- Audit rights written into contracts

- Incident triggers that require vendor notification and response

- Treating vendor artifacts as machine-readable compliance inputs, not marketing materials

The traditional vendor-client dynamic - where the vendor delivers a product and the institution accepts it - does not hold under AI governance. Shared accountability for outcomes is the emerging standard, and institutions should be negotiating for it in contracts now.

Integrating Pillars Into Existing ERM

Building a separate AI governance system alongside existing Enterprise Risk Management creates duplicate forums, diffuses accountability, and fragments control ownership. AI risks should flow into the same risk appetite statements, limits, and issue management processes as operational, cyber, and model risk. The governance structure already exists - the work is extending it to cover AI-specific scenarios.

Operationalizing AI Governance: From Policy to Execution

The Infrastructure Gap

Most institutions have governance blueprints. The problem is that governance failures in AI are almost always infrastructure failures. Controls documented in a policy binder that are not mapped to actual systems, enforced in pipelines, or capable of producing audit-ready evidence are controls in name only.

The 82% of banking leaders who lack confidence in their AI controls are not, in most cases, missing policies. They are missing the operational infrastructure to demonstrate those policies work.

Risk Tiering at Intake

Before any AI use case moves into development, it needs a risk tier. A practical intake process evaluates:

- Acceptable risk - screen out uses that fall outside institutional risk appetite entirely

- AI type - generative, agentic, or conventional ML carry different governance requirements

- Impact classification - consumer-facing, credit-influencing, or fraud-related decisions require deeper pre-development review

High-risk use cases (credit decisioning, fraud alerts, customer-facing interactions) warrant robust oversight before development begins. Internal analytics tools with low consumer impact can follow a faster path. Proportionality is the principle: avoid overengineering low-risk applications while ensuring consequential systems receive the scrutiny they require.

The CRI's AI Adoption Stage Questionnaire evaluates six dimensions - Business Impact, Governance, Deployment Model, Third-Party AI Use, Organizational Goals, and Data Sensitivity - and provides a practical starting point for this tiering.

Embedding Controls Across the Full Lifecycle

Controls cannot concentrate only at deployment. They need to operate at every stage:

- Design phase: risk appetite alignment, architecture review, data preparation, lineage documentation

- Development: secure coding practices, prompt evaluation, adversarial testing

- Deployment: compliance gates, rollback mechanisms, feature flags, kill-switch protocols

- Production: drift detection, anomaly alerting, fairness monitoring, cost surveillance

Cybic's Drava platform supports this lifecycle approach by connecting enterprise data, ML and data science, AI reasoning, and intelligent agents within a governed framework - giving teams the visibility needed to enforce controls at every stage, not just at deployment.

Testing and Incident Readiness

Governance without tested incident response is governance that fails when it matters most. Institutions should build:

- Prompt testing and red-teaming to verify guardrails hold under adversarial conditions

- Regression testing so model or prompt updates do not degrade safety or fairness unnoticed

- AI-specific incident playbooks covering toxicity, data leakage, abnormal cost spikes, and performance drift

- Pre-defined decision rights - who activates the kill switch, who communicates with customers, and under what conditions

The FSSCC's Financial Sector AI Deliverable Reference and Application Guide includes AI fraud incident response playbooks and fraud defense modernization guidance as part of the coordinated AIEOG deliverable set.

Governance Committee and Operating Model

Incident readiness only holds when decision rights are clear. That clarity comes from formalizing the three-lines structure for AI:

- First line builds, deploys, and performs self-assessment

- Second line governs, challenges, and sets standards

- Third line provides independent assurance

The AI governance committee needs a charter with defined decision rights and performance metrics that measure actual effectiveness, not just process activity. Useful metrics include:

- Time to risk assessment completion

- Control test pass rates

- Explainability coverage by use case tier

- Bias metrics across protected classes

- Time to detect and remediate incidents

Managing the Evolving Risk Landscape in 2026

Explainability and Consumer Protection

Explainability is no longer a technical nicety for data science teams. It is a consumer protection requirement with direct regulatory teeth. Under ECOA, FCRA, and UDAAP, AI-influenced decisions affecting consumers must be communicable and contestable.

Operationally, institutions must address this before an examination surfaces the gap:

- Define explainability thresholds for each use case tier

- Document how decisions are made in audit-ready form

- Establish communication protocols for disclosing AI-influenced outcomes to consumers

AI-enhanced fraud has also escalated the threat landscape. FinCEN's November 2024 alert on deepfake-driven fraud schemes provides specific red-flag guidance for financial institutions. The FBI's 2025 Internet Crime Report found that cyber-enabled crimes - including AI scams - defrauded Americans of nearly $21 billion.

The FSSCC's identity deliverable identifies three attack vectors institutions must address:

- Deepfake-driven social engineering

- Synthetic identity creation

- AI agents operating as attack surrogates

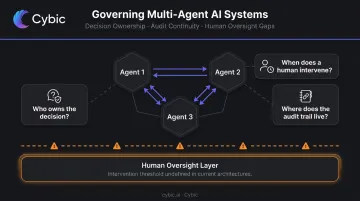

Agentic AI: Governance's New Frontier

Single-model deployments are relatively tractable governance problems. Multi-agent systems are not.

When multiple specialized AI models communicate, synthesize findings, and take autonomous action, the governance questions multiply:

- Who owns a decision that emerged from agent coordination?

- Where does the audit trail live?

- At what point does a human intervene?

Federal Reserve Vice Chair for Supervision Michelle Bowman noted in May 2026 that revised model risk guidance explicitly does not cover generative AI or agentic AI - creating a governance gap that institutions must fill through broader risk management and supervisory discipline. For financial institutions deploying agentic AI in AML, KYC, fraud, and compliance workflows, governance frameworks must account for emergent agent behavior, not just static model outputs.

Human Oversight, Culture, and Organizational Readiness

Regulatory acceptance of AI in financial services remains contingent on meaningful human oversight for consequential decisions. The practical question is not whether humans are involved - it is where their involvement is proportionate to the risk.

Functions that support fuller automation (with appropriate monitoring):

- Initial document review and classification

- High-volume transaction screening

- Routine data processing and aggregation

Functions requiring human judgment:

- Credit denials and adverse action determinations

- Fraud escalations with consumer impact

- Suitability or investment recommendations

- Any decision where contextual understanding or accountability is legally required

FINRA Regulatory Notice 24-09 is explicit on this point for securities firms: using generative AI does not change existing supervisory obligations under Rule 3110.

Meeting those obligations depends as much on organizational culture as on technical controls - and that culture tends to receive less investment than it deserves.

Building Shared AI Literacy Across Teams

Data scientists, engineers, risk managers, compliance officers, legal counsel, and operations teams all need enough shared AI literacy to collaborate on governance without constant translation overhead. Shared artifacts close that gap: model cards, risk assessment templates, prompt libraries, and red-team playbooks give cross-functional teams a common reference point.

Embedding risk partners early in the design process is equally important. When they're involved from the start, evidence generation becomes routine rather than a scramble conducted under examination pressure.

Frequently Asked Questions

What is the Financial Services AI Risk Management Framework (FS AI RMF)?

Released by the Cyber Risk Institute on February 12, 2026, the FS AI RMF was built with FSSCC and more than 100 financial institutions and announced by Treasury as part of the AIEOG deliverable series. It adapts the NIST AI RMF into 230 control objectives spanning governance, model development, third-party risk, and consumer protection - giving institutions practical, examination-oriented tools.

How does AI governance differ from traditional model risk management?

Traditional model risk management (SR 11-7) focuses on statistical validity and model performance. AI governance is broader: it covers data lineage, fairness, explainability, identity controls, third-party AI risk, agentic behavior, and continuous lifecycle monitoring. OCC Bulletin 2026-13 confirms that revised model risk guidance explicitly excludes generative AI and agentic AI, meaning institutions must extend governance beyond what MRM frameworks were designed to address.

What does Treasury's 2026 AI guidance require of financial institutions?

Treasury's AIEOG guidance spans six deliverables - including the FS AI RMF, AI Lexicon, explainability guidance, and fraud and identity materials - and sets clear supervisory expectations. AI risk must be embedded in existing ERM frameworks, controls must map to specific systems, and institutions must produce evidence artifacts demonstrating effectiveness, not just policy documentation.

What are the biggest AI governance risks financial institutions face in 2026?

The primary risks in 2026 include:

- AI-enhanced deepfake identity attacks and synthetic fraud

- Hallucination and data leakage from generic LLMs

- Lack of defensible explainability for consumer-facing decisions

- Governance debt from shadow model development and fragmented data ownership

- Accountability gaps from autonomous multi-agent systems in AML, KYC, and fraud workflows

How do financial institutions operationalize AI explainability?

Institutions need to define explainability thresholds proportional to the regulatory context of each use case, document decision logic in audit-ready artifacts, and establish communication protocols for disclosing AI-influenced outcomes to consumers. Explainability evidence should be integrated into standard control testing cycles - not treated as a separate compliance exercise triggered only by examination or complaint.

When does AI governance require human-in-the-loop oversight?

Human oversight is most critical for high-impact decisions - credit denials, fraud escalations, and suitability determinations - where AI cannot provide contextual judgment or bear legal accountability. Routine screening and initial document review can be automated with appropriate monitoring controls. Any decision with material consumer or regulatory consequence needs a defined human sign-off requirement set before deployment, not after an incident.