Introduction

According to McKinsey's November 2025 survey, 23% of organizations are already scaling agentic AI systems enterprise-wide and another 39% are actively experimenting. After years of chatbots and pilot programs, financial services has moved into the execution phase. Banks, insurers, and wealth managers are deploying autonomous systems that plan, act, and adapt across complex multi-step workflows.

The pressure to act is real. Financial institutions face macroeconomic volatility and fintech disruption while operating under some of the world's strictest regulatory constraints. Financial services firms spent $35 billion on AI in 2023, with investments projected to reach $97 billion by 2027. The question is no longer whether to adopt agentic AI, but how to do it without creating new operational or compliance risks.

This guide covers what agentic AI actually is, how leading banks are deploying it, and the use cases reshaping compliance, fraud detection, and customer service. It also lays out the governance requirements and implementation framework you need to deploy it responsibly.

TLDR:

- Agentic AI autonomously plans, executes, and adapts multi-step financial workflows with minimal human intervention

- Leading banks like JPMorgan Chase have scaled AI agents to over 200,000 employees within eight months

- KYC automation cuts source-of-wealth report generation from 10 days to 1 hour

- AI-driven fraud detection reduces false positives by 45% and investigative time by 60%

- Governance must be embedded at the architectural level and not added post-deployment

What Is Agentic AI in Financial Services?

Agentic AI represents a fundamental shift from passive prediction to autonomous execution. Traditional AI classifies transactions or predicts credit risk within fixed parameters. Generative AI creates content from prompts but stops there. Agentic AI goes further: it plans workflows, makes decisions, takes action, and adapts based on real-time feedback without waiting for human instruction at each step.

Three Defining Characteristics:

- Executes tasks independently, without requiring human input at every step

- Learns continuously from new data, outcomes, and environmental changes

- Coordinates with other agents, APIs, and financial databases to complete workflows no single model could handle alone

How Agentic Architecture Works

According to IEEE's January 2026 definition, agentic AI systems "represent knowledge, reason, plan, act, learn, and adapt within complex, dynamic, and open-ended environments." In practice, this means orchestrator or supervisory agents manage processes by assigning tasks to specialized sub-agents, each trained on a specific domain.

For example, in loan processing, a supervisory agent might coordinate specialized sub-agents that handle:

- Credit scoring

- Income verification

- Fraud detection

- Risk modeling

- Automated approval recommendations

AWS describes this as a hierarchical topology where borrower documentation flows through specialized agents in sequence, with each agent completing its designated task before passing results to the next in the chain.

That architectural model maps naturally onto how financial institutions already operate which is why the sector is particularly well-suited for agentic deployment.

Why Financial Services Is Ideal for Agentic AI

Financial services offers uniquely favorable conditions for agentic deployment:

- Data-rich operations with mature APIs and process orchestration

- Repetitive high-volume workflows in compliance, KYC, and claims processing

- Real-time risk assessment requirements in trading and fraud detection

- Growing imperative to personalize services at scale across mass-market segments

- Established authorization, privacy, and security controls that agents can integrate with

Gartner notes that financial services workflows feature "high-volume interactions, transactions and context... mature data, metadata, APIs, workflows and process orchestration... [and] established authorizations, privacy, trust and security controls" , conditions that few other industries can match at the same scale.

Key Use Cases of Agentic AI in Financial Services

Agentic AI reaches across banking, insurance, wealth management, and capital markets reshaping core workflows in each domain rather than solving a single isolated problem.

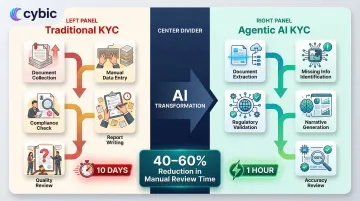

KYC, Compliance, and Onboarding Automation

Know Your Customer (KYC) processes have long been bottlenecks. Average annual spend on AML/KYC operations now stands at $72.9 million per firm, and 70% of financial institutions lost clients in the past year due to slow onboarding the highest rate ever recorded.

Agentic AI reimagines KYC as an end-to-end automated process:

- Extracts data from documents

- Identifies missing information

- Validates against regulatory requirements

- Generates source-of-wealth narratives

- Reviews narratives for accuracy

Real-world impact:

- Bank of Singapore cut source-of-wealth report preparation from 10 days to 1 hour using its AI agent-powered Source of Wealth Assistant

- A global Tier-1 bank achieved 40-60% reduction in manual document review time, saving hundreds of analyst hours per week

This frees compliance analysts to focus on high-complexity judgment work rather than manual data processing.

Fraud Detection and Financial Crime Prevention

Traditional rule-based AML systems suffer from 85-95% false positive rates, meaning most compliance alerts don't represent genuine financial crime risk. Meanwhile, fraud's impact has increased 25% since 2021, now averaging more than $5 for every $1 lost to fraud.

Agentic AI shifts fraud defense from reactive pattern-matching to proactive multi-signal reasoning:

- Monitors transactions in real time

- Cross-references external databases

- Identifies non-obvious networks of suspicious activity

- Escalates cases while continuously refining models

Proven results: After implementing AI-driven risk scoring, one bank reduced false positives by 45% and investigative time by 60%.

The key advantage: agentic AI coordinates across internal and external data sources simultaneously, making it harder for sophisticated financial crime networks to evade detection through fragmented signals.

Algorithmic Trading and Real-Time Risk Management

AI agents autonomously monitor market conditions, detect correlations, trigger pre-approved trades, and dynamically adjust risk parameters in response to live data reducing the latency between insight and action in volatile markets.

In credit risk, agentic AI continuously evaluates borrower solvency using real-time data streams rather than static periodic reviews. Upstart's AI model provides about 5X more risk separation than FICO, enabling more accurate risk-based pricing. In 2024, more than 91% of Upstart-powered loans were fully automated with instant approvals.

Customer Service, Personalized Advice, and Agentic Payments

Agentic AI lets financial institutions deliver tailored guidance across account management, loan processing, and dispute resolution at scale services previously reserved for high-net-worth clients. The opportunity is real: only 9% of the UK population paid for financial advice in the last two years, leaving 91% of consumers without structured support.

Agentic payments take this further. AI agents autonomously initiate, authorize, and complete transactions on a customer's behalf based on pre-defined conditions automatically refinancing a mortgage when rates drop, or rebalancing a portfolio when thresholds are triggered.

Real-world frameworks:

- Mastercard's Agent Pay integrates with agentic AI to enable AI agents to securely execute transactions using tokenized credentials

- Visa's Intelligent Commerce opens Visa's payment network to developers building foundational AI agents transforming commerce

Both launched in April 2025, signaling that agentic payments are moving from concept to production infrastructure. Together, these four use cases show how agentic AI is progressing from targeted automation into core financial infrastructure.

Which Banks Are Using Agentic AI?

JPMorgan Chase: Leading at Scale

JPMorgan Chase's LLM Suite went from zero to 200,000 onboarded employees within eight months after launching in summer 2024. The platform gives eligible employees secure access to large language models across the firm.

Plans include integrating internal data sources and combining generative AI with workflows to build agents that complete multi-step goals autonomously.

JPMorgan is investing heavily: $18 billion tech budget for 2025, with AI expected to drive efficiencies that could reduce headcount by 10% in some operations over five years.

Other Major Global Banks

Citi: Deploying agentic AI capabilities to employees via its Citi Stylus Workspaces platform, starting with a pilot of 5,000 workers. Employees can now conduct in-depth research, extract insights from vast datasets, and streamline multi-stage workflows into single automated processes.

HSBC: Partnered with Mistral AI in December 2025 to enhance generative AI use across the bank, with future focus on customer-facing innovations including credit and lending processes, customer onboarding, and fraud and anti-money laundering checks.

Internal-First Deployment Pattern

A consistent pattern emerges among early adopters: they start with employee-facing or internal use cases like software engineering, compliance, data operations prove ROI, then expand to client-facing workflows. This sequencing is deliberate, a risk-managed path to scaling AI across regulated operations.

The gap between leaders and laggards is widening. Institutions that have moved beyond pilots into scaled deployments are compounding operational advantages that proof-of-concept programs cannot match.

The Business Case: Benefits and Efficiency Gains

Quantified Productivity Improvements

McKinsey estimates AI could bring gross reductions of as much as 70% in certain cost categories, with net effects on banks' aggregate cost base representing a 15-20% decrease after accounting for rising technology costs.

KYC-specific gains:

- 30-50% reduction in handling time

- Fewer false positives

- Lower per-case compliance cost

Deloitte predicts AI tools will help save 20-40% in software investments for banking by 2028, with per-engineer cost savings of $0.5 million to $1.1 million.

Strategic Value Beyond Cost Savings

Those cost reductions only tell part of the story. Agentic AI changes what's possible at scale institutions can grow service capacity without growing headcount at the same rate.

In practice, this plays out across three operational areas:

- Service scaling: Handle higher transaction volumes and client interactions without adding staff proportionally

- Personalization: Deliver tailored product recommendations and risk assessments across millions of customers simultaneously

- Market responsiveness: Adjust credit models, fraud thresholds, or pricing parameters in near real-time as conditions shift

Expanding Financial Inclusion

AI can accelerate financial inclusion by extending access to formal financial services for underserved populations. Alternative data-based credit scoring reaches applicants with no traditional credit history, while automation lowers the cost-to-serve enough to make smaller accounts economically viable.

Governance, Risk, and Compliance in Agentic AI

Why Agentic AI Governance Is Different

Governance for agentic AI demands a different architecture than traditional AI governance. Autonomous agents chain actions with downstream consequences which means auditability, explainability, and override mechanisms must be built into system architecture from the start, not retrofitted afterward.

Regulatory Requirements

The EU AI Act entered force August 1, 2024, and will be fully applicable August 2, 2026. High-risk AI providers must:\n- Establish risk management systems\n- Conduct data governance\n- Draw up technical documentation\n- Design systems for record-keeping\n- Implement human oversight capabilities

The US Treasury's Financial Services AI Risk Management Framework addresses concerns that accelerated AI adoption creates complex risks not clearly addressed by traditional frameworks, particularly for emerging agentic systems.

Financial regulators will likely demand:\n- Transparent decision-tracking for AI-driven credit or compliance actions\n- Role-based access controls limiting what agents can autonomously execute\n- Clear accountability frameworks when AI-driven decisions cause harm\n- Continuous monitoring to detect model drift in production

Security and Legacy Integration Challenges

The TD Bank case makes the data infrastructure problem concrete. When AI agents operate on poor-quality or fragmented data, errors don't stay isolated, they propagate at speed and scale across every process those agents touch.

The TD Bank enforcement action in October 2024 illustrates this risk. TD Bank's AML senior management concluded that only proposed changes "that would have no impact or lower the volume of false positives have been approved to proceed" , meaning the system couldn't add new high-risk jurisdictions because doing so would increase alert volume. This created blind spots that enabled financial crime.

Institutions with fragmented legacy infrastructure face the same trap: clean, interconnected data is a prerequisite and not a nice-to-have before deploying autonomous agents at scale.

Governance-Embedded Design

Architecting security controls, RBAC, encrypted data handling, and audit trails into AI systems from the ground up is the most defensible approach. As JPMorgan Chase notes:

"Controls must operate at the point of execution and produce tamper-evident, complete runtime records to support audits, investigations and incident response."

A governance-by-design architecture typically covers:

- Access controls: Role-based permissions limiting what each agent can read, write, or execute

- Encrypted data handling: Protection in transit and at rest, with strict data governance

- Auditability: Tamper-evident logs of every AI-driven action and decision

- Traceability: End-to-end visibility into how agents reached a given output

Cybic's Drava platform is built on this model governance, access controls, and auditability are embedded at the architectural level rather than layered on after deployment. That distinction matters when regulators and internal risk teams are reviewing how decisions were made and who had authority to make them.

How to Implement Agentic AI in Financial Services

Start with High-Value, Lower-Risk Internal Use Cases

Begin with compliance support, document processing, or software engineering to:

- Build confidence in AI capabilities

- Generate measurable ROI

- Develop internal AI fluency

Only then expand to client-facing applications. JPMorgan and Citi both took this path starting with internal compliance and operations tools before deploying AI in client-facing workflows.

Infrastructure and Data Prerequisites

Agentic AI requires modern, interconnected data systems. Before deployment:

Audit your data architecture:

- Ensure model outputs are traceable to source data

- Confirm infrastructure can support real-time inference

- Verify data quality and completeness

Cloud-native or hybrid deployments offer the flexibility agentic workloads require low latency, real-time inference, and the ability to scale without rebuilding your stack.

Human-Centered Change Management

Technology deployment is only part of the equation. Institutions must:

- Invest in training across leadership and operational teams

- Embed AI literacy into ongoing team workflows and not just onboarding

- Design human-in-the-loop checkpoints for high-stakes decisions

- Establish clear escalation protocols

Institutions that don't want to build this capability from scratch often work with an AI engineering partner like Cybic, which integrates governance, compliance requirements, and deployment infrastructure into the system architecture from day one and not as an afterthought.

Frequently Asked Questions

What is agentic AI in financial services?

Agentic AI refers to autonomous AI systems capable of planning, executing, and adapting multi-step tasks in financial workflows with minimal human intervention. Unlike traditional AI (which predicts) or generative AI (which creates content), agentic AI combines reasoning, decision-making, and execution toward complex goals.

How is agentic AI used in financial services?

Primary applications include KYC and compliance automation, fraud detection, credit risk assessment, algorithmic trading, personalized customer advice, and autonomous payment execution. These systems handle everything from document verification to real-time transaction monitoring and portfolio rebalancing.

How can agentic AI change the way banks fight financial crime?

Agentic AI moves fraud defense from reactive rule-matching to proactive, multi-signal reasoning. Agents continuously monitor transactions, cross-reference data sources, and identify coordinated criminal networks in real time reducing false positives by up to 45% while cutting investigative time by 60%.

What are agentic AI payments?

Agentic AI payments are AI-driven systems that autonomously initiate, authorize, and complete financial transactions on a user's behalf based on pre-set conditions. Examples include Mastercard's Agent Pay and Visa's Intelligent Commerce, both launched in April 2025 to enable secure AI-driven commerce.

Which banks are using agentic AI?

Leading adopters include JPMorgan Chase (200,000+ employees using LLM Suite), Citi (deploying agentic tools via Stylus Workspaces), and HSBC (partnering with Mistral AI). Production deployments are now standard across top-tier institutions, spanning KYC, trading, and customer service.

How big is the agentic AI in the financial services market?

Financial services firms spent $35 billion on AI in 2023, with projected investments expected to reach $97 billion by 2027 projected to reach $97 billion by 2027 across banking, insurance, capital markets, and payments.