Introduction

AI is no longer a back-office experiment in financial services - it's making credit decisions, flagging fraud, onboarding clients, and generating research output at scale. And regulators have noticed.

According to Deloitte's 2025 financial institution survey, two-thirds of banks and insurers were using AI or ML by 2025, with small-bank adoption jumping from 22% to 52% in just two years. GenAI adoption hit 94% at large banks. Yet more than half of those same institutions cited transparency and explainability as a governance hurdle they hadn't fully solved.

The gap between deployment velocity and governance readiness is where regulators are focusing. FINRA, the SEC, CFPB, and NYDFS aren't waiting for AI-specific legislation - they're applying existing supervision, recordkeeping, fair-lending, and cybersecurity rules to AI systems right now.

That pressure makes governance a strategic priority, not just a compliance checkbox. This article covers the five trends reshaping financial services AI governance in 2026, what's driving them, and how to build a framework that holds up under examiner scrutiny.

Key Takeaways

- Two-thirds of banks use AI or ML, but most governance programs haven't kept pace with deployment

- Regulators are applying existing rules - recordkeeping, fair-lending, supervision - to AI decisions without waiting for new legislation

- Agentic AI requires an entirely different governance model than static tools or employee-facing assistants

- Shadow AI follows the off-channel communications enforcement pattern - regulators don't need new rules to act on it

- Governance-embedded-by-design produces exam-ready systems; retrofitted controls produce gaps

Key AI Governance Trends Reshaping Financial Services Compliance in 2026

Trend 1: Agentic AI Introduces a New Class of Governance Requirements

Agentic AI isn't a smarter chatbot. These are systems that execute multi-step tasks autonomously - processing a loan application end-to-end, triaging a suspicious transaction, or orchestrating a client onboarding workflow without waiting for human input at each step.

The governance problem is structural. Traditional model risk management assumes a human initiates an action and a model produces an output. Agentic systems break that assumption. One prompt can trigger a chain of downstream decisions, data lookups, and external system calls - each of which may touch regulated processes.

FINRA's 2026 Annual Regulatory Oversight Report explicitly flags GenAI and agentic systems as supervision, recordkeeping, and fair-dealing concerns for broker-dealers. In a separate FINRA blog on AI agents, the regulator notes that agentic AI has moved from conceptual discussion into early practical deployment among member firms - and that current supervisory frameworks weren't designed for it.

What agentic governance requires, specifically:

- Every agent action traced back to an initiating human identity

- Policy enforcement applied at each step in the workflow, not just at the prompt level

- Full end-to-end reconstruction capability for any autonomous sequence

- Documented supervisory procedures updated to cover agent behavior under FINRA Rule 3110

Firms deploying agentic AI in credit underwriting, fraud triage, or onboarding workflows that haven't updated their supervisory procedures are carrying unquantified regulatory exposure.

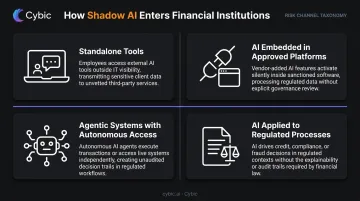

Trend 2: Shadow AI Becomes Financial Services' Biggest Compliance Blind Spot

Shadow AI is what happens when employees use AI tools that the firm never approved, never reviewed, and never configured for compliance. Think ChatGPT drafting a client summary, or an AI embedded in a project management tool summarizing a meeting that discussed non-public information.

The enforcement parallel is direct. In August 2024, 26 broker-dealers and investment advisers paid $392.75 million combined for failing to preserve electronic communications conducted through off-channel platforms. The underlying problem wasn't malicious intent - it was employees using convenient tools that the firm's supervision infrastructure couldn't see. Shadow AI recreates that exact scenario.

A 2025 Gartner survey of 302 cybersecurity leaders found 69% of organizations suspect or have evidence that employees are using unapproved GenAI tools. In financial services, where every client interaction is potentially a regulated communication, that number represents significant unmonitored exposure.

Shadow AI enters firms through four channels:

- Standalone tools - employees using ChatGPT or similar tools directly, outside any firm-sanctioned environment

- AI embedded in approved platforms - Microsoft Copilot, Salesforce Einstein, or similar AI features inside tools that IT approved before the AI layer was added

- Agentic systems with autonomous access - AI that connects to firm data through integrations that weren't designed with supervision in mind

- AI applied to regulated processes - research analysts using AI for report drafting, advisors using it for client communications

The compliance exposure: regulated data and client communications flowing into unvetted tools, unretained and unsupervised, that firms cannot produce during an examination.

Trend 3: Regulators Now Expect Audit Trails and Explainability

The SEC's FY2026 examination priorities are specific: examiners will review whether firms have adequate policies and procedures to monitor AI technologies, and whether AI representations to clients are accurate. The scope covers automated investment tools, trading algorithms, fraud detection, AML functions, and back-office AI.

The evidentiary standard behind that scope is getting harder to meet.

Traditional DLP and CASB tools were built for content inspection and file-level controls. They tell you what data left the network. Examiners increasingly want to understand what happened inside an AI interaction - what was entered, what the model returned, what controls were applied, and what disposition resulted. Firms that can't reconstruct that sequence face a documentation gap that can't be papered over after the fact.

Explainability operates at two levels:

- Regulatory: Examiners expect documented evidence of AI behavior, controls, and outcomes for any AI-driven function in scope

- Customer-facing: The CFPB's Circular 2022-03 confirmed that ECOA adverse-action notice requirements apply equally to complex algorithm-based credit decisions - meaning if AI denies a loan application, the institution must be able to produce specific, articulable reasons for that outcome

Opaque models that can't generate reason codes aren't just a technology problem. They're an ECOA compliance problem.

Trend 4: Model Risk Management Expands Beyond SR 11-7

SR 11-7 governed quantitative models for 15 years. It wasn't designed for AI systems that retrain, drift, and can embed historical bias at scale.

On April 17, 2026, the Federal Reserve issued SR 26-2, superseding SR 11-7. The update is significant in two ways: it introduces updated continuous monitoring requirements for covered models, and it explicitly excludes generative AI and agentic AI from its scope, categorizing them as "novel and rapidly evolving." That exclusion doesn't mean those systems are ungoverned. It means institutions need to build a separate governance layer for GenAI and agentic AI that SR 26-2 doesn't provide.

The practical risks this creates:

- A credit model trained on historically biased lending data can perpetuate discrimination at scale before drift or disparate impact is detected

- A fraud detection model calibrated during stable economic conditions may generate excessive false positives during a market shock

- Vendor-supplied AI models carry institutional accountability regardless of who built them - SR 26-2 preserves this principle, requiring banks to understand conceptual soundness, monitor performance, and conduct ongoing outcome analysis even when they don't have access to the underlying code

Third-party AI vendor risk management is no longer optional paperwork. It's a documented examination expectation.

Trend 5: Governance-Embedded-by-Design Replaces Compliance as an Afterthought

The firms that retrofitted governance after deployment are discovering what that approach actually costs: fragmented audit trails, access controls that don't match risk tiers, and documentation gaps that surface exactly when examiners ask for them.

Governance-embedded-by-design inverts that sequence. Access controls, data encryption, audit logging, bias monitoring, and regulatory alignment are built into the AI architecture before the first production query runs.

In practice, this means:

- Enforce role-based access controls (RBAC) that govern who can query, modify, or retrain AI models

- Protect data with encryption in transit and at rest across all deployment environments

- Capture full interaction context for every AI-driven action - not just that something happened, but enough detail to reconstruct it

- Prevent proprietary enterprise data from being used to train external models through strict data governance policies

- Maintain consistent governance behavior across cloud, hybrid, and on-premises environments

Cybic's Drava platform is built around this architecture. Drava embeds RBAC, encrypted data protection, auditability, and responsible AI frameworks directly at the architectural level - so financial institutions can demonstrate compliance at any point in the AI lifecycle, not only at the moment of deployment.

What's Driving These AI Governance Trends

Regulatory Pressure Is Coming From Multiple Directions Simultaneously

Regulators aren't waiting for a unified AI law. They're applying existing frameworks to AI systems right now:

- FINRA Regulatory Notice 24-09 (June 2024) confirmed that existing FINRA rules on supervision, recordkeeping, communications, and fair dealing apply directly to GenAI and LLM use

- SR 26-2 (April 2026) supersedes SR 11-7, updates continuous monitoring expectations, and creates a governance gap for GenAI and agentic AI that institutions must fill independently

- NYDFS 23 NYCRR 500 applies to cybersecurity risk management, with a 2024 industry letter addressing AI-specific cybersecurity exposures without requiring new rulemaking

- Colorado SB24-205 creates duties for deployers of high-risk AI systems used in consequential decisions - adding state-level obligations that don't wait for federal action

- EU AI Act classifies creditworthiness AI as high-risk - its risk-based framework is already influencing how US regulators think about tiering AI oversight

Each of these frameworks carries distinct scope, enforcement mechanisms, and timelines. Firms must map every applicable obligation to their specific AI use cases, jurisdictions, and deployment environments - and the mapping is rarely clean.

Deployment Velocity Is Outpacing Governance Readiness

That regulatory complexity doesn't slow adoption - it collides with it. Small-bank AI adoption more than doubled in two years, while large banks reached 94% GenAI adoption. Institutions building compliance programs to match that pace are ahead; those treating governance as a post-deployment exercise are falling behind in real time.

Competitive pressure compounds this further. Institutions that delay AI adoption cede ground to faster-moving competitors. Deploying quickly and governing simultaneously - not sequentially - is the defining operational challenge of 2026.

How These Trends Are Impacting Financial Institutions

Operational Impact

Compliance teams must now extend supervision frameworks to AI-generated content - meeting summaries, research outputs, credit determinations, client communications. These aren't document-centric records. They're interaction-level outputs that require capture, retention, and review aligned with the same standards as human-authored records.

Moving from document oversight to interaction oversight isn't a policy tweak. It restructures how compliance teams scope their work, assign accountability, and configure their recordkeeping systems.

Business and Workforce Impact

Financial institutions are responding with structural investment:

- Cross-functional AI governance committees spanning compliance, legal, technology, business lines, and data privacy

- Formal AI model inventories with risk tiering, approval gates, and change documentation

- PwC's 2025 Responsible AI survey found that 56% of executives report first-line teams - IT, engineering, data science - now lead responsible AI efforts, reflecting how deeply governance has moved into technical delivery

The talent gap is real. Compliance officers need sufficient model risk literacy to ask the right questions. Data scientists need compliance literacy to build auditable systems. That intersection is where most institutions are understaffed.

Building an AI Governance Framework That Satisfies Regulators in 2026

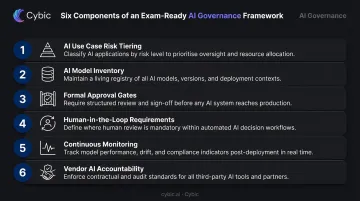

Regulatory expectations in 2026 have moved past policy statements. Examiners want operational evidence - documented controls, testable processes, and clear accountability at every layer of the AI lifecycle. A credible governance framework has six components that deliver exactly that:

1. AI use case risk tiering Separate high-stakes applications (credit decisioning, fraud detection, customer segmentation, AML) from lower-risk automation. Risk tier determines governance control intensity, testing requirements, and monitoring frequency.

2. Maintained AI model inventory Document each system's use case, data sources, algorithm logic or approach, validation results, and monitoring metrics. SIFMA's guidance recommends inventories detailed enough to support risk rating.

3. Formal approval gates New deployments and material changes require documented review - technical validation, compliance sign-off, and risk tier confirmation before production.

4. Human-in-the-loop requirements For regulated decisions - loan denials, fraud flags, investment recommendations - define explicit review requirements, escalation paths, and override documentation.

5. Continuous monitoring Establish baseline performance metrics pre-production. Define acceptable deviation thresholds. Automate monitoring for model drift, performance degradation, and disparate impact across demographic cohorts. Document escalation and remediation workflows.

6. Vendor AI accountability Require documentation, validation results, ongoing monitoring agreements, and audit rights for every third-party AI model - SR 26-2 and interagency third-party guidance preserve full institutional accountability regardless of vendor origin.

Cybic engineers this framework directly into client architectures through the Drava platform. Rather than adding compliance controls after deployment, Drava embeds them at the infrastructure level - across cloud, hybrid, and on-premises environments - covering:

- Role-based access controls (RBAC) for system-level security

- AES-encrypted data protection in transit and at rest

- Full auditability and traceability of AI-driven actions

- A strict no-training-on-proprietary-data policy

Financial institutions get governance that regulators can examine, not a compliance layer bolted on after the fact.

Future Signals for AI Governance in Financial Services

The governance bar will continue rising. Three developments are worth tracking:

- FINRA agentic AI guidance: FINRA is actively observing member firm agentic AI deployments. Prescriptive rules on agent identity attribution and multi-step workflow documentation are likely within 1–2 years - institutions that build those capabilities now avoid a compliance retrofit later

- EU AI Act influence: The Act classifies creditworthiness AI as high-risk, with transparency, human oversight, and accuracy requirements. As US regulators develop more prescriptive AI frameworks, the EU's risk-based model is the most likely template

- AI monitoring AI: Automated compliance systems that monitor AI decisions and flag violations in real time are moving from concept to production use - governance infrastructure investment here delivers operational returns, not only risk mitigation

Institutions that invest in governance infrastructure now - model inventories, audit trail depth, agentic controls, and workforce training - shift from defensive compliance to competitive differentiation. That maturity translates into concrete advantages:

- Wins enterprise clients who require demonstrated governance standards

- Accelerates regulatory examinations with audit-ready documentation

- Expands AI use cases that ungoverned architectures cannot support

Competitors that skip this groundwork will face enforcement actions that are, by now, entirely predictable.

Frequently Asked Questions

What is AI governance in financial services?

AI governance in financial services is the set of policies, controls, and oversight mechanisms ensuring AI systems meet regulatory standards for transparency, fairness, and explainability. It spans model development, testing, production monitoring, audit trail management, and vendor accountability across every AI-driven function.

What regulations govern AI use in US financial services in 2026?

No single AI law governs - existing frameworks apply across the board. Key rules include FINRA Regulatory Notice 24-09, FINRA's 2026 oversight priorities, SEC FY2026 exam priorities, SR 26-2 (replacing SR 11-7 in April 2026), NYDFS 23 NYCRR 500, GLBA, CFPB Circular 2022-03, and Colorado's state-level AI legislation.

What is shadow AI and why is it a compliance risk?

Shadow AI is employees using unapproved AI tools outside firm-sanctioned governance frameworks. It's a compliance risk because regulated data and client communications flowing through unvetted tools aren't captured, supervised, or producible during exams, mirroring the off-channel communications failures that cost 26 firms $392.75 million in 2024.

How does agentic AI change compliance requirements?

Agentic AI executes multi-step tasks autonomously, requiring governance that traces every action to a human identity, enforces policy at each workflow step, and produces full end-to-end reconstruction. That goes well beyond the prompt-level monitoring sufficient for traditional AI tools.

What is model drift and why does it matter for compliance?

Model drift occurs when AI accuracy degrades as market conditions or data patterns change, potentially causing biased credit decisions or excessive fraud false positives. SR 26-2 requires ongoing monitoring and documented remediation processes for covered models, and institutions need equivalent controls for GenAI and agentic systems, which SR 26-2 explicitly excludes from its scope.

How does governance-embedded-by-design differ from bolted-on compliance?

Governance-embedded-by-design means access controls, encryption, auditability, and regulatory alignment are built into AI architecture from inception, not added after deployment. The result is systems that are compliant-by-construction, with audit evidence available at any point in the AI lifecycle.