Introduction

Financial services consulting is undergoing a structural redesign. How analysis gets done, how compliance gets managed, how risk gets priced, and how clients get served are all being rebuilt from the ground up.

McKinsey estimates generative AI could add $200 billion to $340 billion in annual value across banking - equivalent to 2.8% to 4.7% of industry revenues. The pressure to act is real.

Financial institutions can't move fast and break things, though. Fiduciary obligations, strict data governance requirements, and regulatory scrutiny make undisciplined AI deployment genuinely dangerous.

This article covers where AI is having the deepest impact on financial services consulting, why governance must be embedded from day one rather than retrofitted later, and what a well-structured AI consulting engagement actually looks like.

Key Takeaways

- AI has moved from narrow automation to core operational infrastructure across fraud, credit, compliance, and customer engagement

- The highest-ROI consulting opportunities are fraud detection, KYC automation, and credit risk modeling - each with documented benchmarks

- Governance built into the architecture separates systems that pass regulatory scrutiny from those that get shelved

- Agentic AI is arriving in financial workflows, but over 40% of agentic AI projects are projected to be canceled by 2027 without proper risk controls

- Effective AI consulting in financial services ends with deployed systems - not roadmaps

From Operational Tool to Strategic Asset: How AI Is Redefining Consulting in Finance

AI in financial services started narrow - algorithmic trading, rule-based credit scoring, basic fraud filters. What's changed is scale and depth. AI is now embedded across the full operational lifecycle: underwriting decisions, compliance monitoring, customer onboarding, product design, and regulatory reporting.

This evolution is changing what consulting actually means.

Traditional engagements delivered strategy decks after months of analysis. That model is being displaced by engagements that deliver working, deployed systems - because AI compresses the distance between insight and execution. Clients don't want a roadmap for where AI could go. They want the system running.

The Competitive Pressure Is Structural

Fintechs accelerated this expectation. Accenture estimates that nearly $550 billion has been invested in fintech since 2010, and while no fintech has entered the global top 250 banks by assets, digital-native competitors permanently reset what customers expect from financial services. Speed, personalization, and seamless digital experience are now baseline requirements.

Institutions that can't match this operationally don't just lose market share to other banks. They lose to leaner, AI-first startups accessing the same advanced capabilities through open-source models, scalable APIs, and cloud-native infrastructure.

Accenture also found that 73% of U.S. bank employee work time is suitable for automation or augmentation by generative AI. That figure isn't a technology opportunity. It's a signal that the operating model itself needs to change - and that change is already underway at institutions moving faster than their competitors.

The practical implications cut across every function:

- Underwriting and credit: AI models now process structured and unstructured data simultaneously, reducing decision cycles from days to minutes

- Compliance monitoring: Continuous transaction surveillance replaces periodic manual review, with audit trails built in

- Customer onboarding: Intelligent document processing and identity verification reduce friction without sacrificing regulatory controls

- Regulatory reporting: Automated data pipelines replace spreadsheet-driven processes that carry significant error risk

Where AI Is Making the Biggest Impact in Financial Services Consulting

Fraud Detection and Financial Crime Prevention

Static, rule-based fraud detection has a fundamental flaw: it can only catch fraud patterns it already knows about. The moment a new typology emerges, the rules fail. Meanwhile, false positive rates in traditional systems are high enough to create significant operational drag and poor customer experience.

Machine learning changes the model. Rather than matching transactions against a fixed ruleset, ML systems learn normal behavioral patterns and flag anomalies - including novel fraud typologies that no rule would catch. The performance improvement is measurable.

HSBC's Dynamic Risk Assessment AI produced 60% fewer false positive cases while processing approximately 980 million transactions per month - and reduced analysis time from several weeks to a few days. For consulting engagements, that's the benchmark to design toward: measurable false-positive reduction at production scale, not just proof-of-concept accuracy.

The stakes justify the investment. UNODC estimates money laundering at 2–5% of global GDP annually - roughly $800 billion to $2 trillion. Financial crime compliance costs U.S. and Canadian institutions $61 billion per year, and Fenergo reported $4.6 billion in global enforcement actions against financial institutions in 2024 alone.

The consulting implication: fraud AI isn't just a technology project. It requires mapping existing AML/KYC workflows, designing model governance frameworks, and ensuring outputs are auditable by regulators. Detection performance matters - but so does explainability.

Credit Risk Modeling and Underwriting

Expert-judgment-based credit decisions have a coverage problem. Roughly 32 million U.S. adults are unscorable using traditional credit data - classified as credit invisible or thin-file consumers. ML models that incorporate transaction history, cash-flow data, and behavioral signals can reach these populations without increasing default rates.

FinRegLab's 2025 research found ML credit models improved ROC-AUC by approximately 2% versus logistic regression. At conservative risk thresholds, these models increased approvals by nearly 4% while reducing approvals of consumers who later defaulted by at least 9%. Wider access and lower losses at the same time - that's what makes the credit AI case so compelling to lenders.

The regulatory challenge is equally substantial:

- Credit scoring AI is classified as high-risk under the EU AI Act (Annex III)

- The CFPB requires specific, accurate adverse-action reasons even when decisions rely on complex algorithms

- The Basel Committee has identified explainability, data quality, and governance as primary AI/ML model risks in regulated credit environments

Consultants must help institutions balance model performance with model transparency. A credit model that works but can't be explained to a regulator is not production-ready.

Compliance, Regulatory Reporting, and KYC Automation

KYC and AML compliance is expensive, manual, and under constant regulatory pressure. KPMG benchmarks a typical KYC/CDD client refresh at 1,200 minutes; their managed-service process cuts that to 400 minutes. One case study showed end-to-end compliance processing drop from 11 hours per case to under 5 hours.

At scale, those gains translate directly to cost reduction and risk exposure reduction. The penalty numbers make the business case clear: $4.6 billion in enforcement actions in 2024, with transaction-monitoring failures accounting for $3.3 billion of that figure.

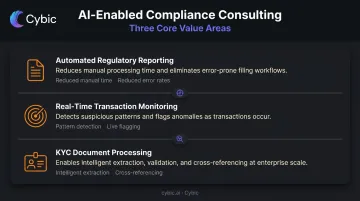

AI-enabled compliance consulting delivers value across three specific areas:

- Automated regulatory reporting - reducing manual preparation time and error rates

- Real-time transaction monitoring - detecting suspicious patterns as they occur, not after batch processing

- KYC document processing - using intelligent document processing to extract, validate, and cross-reference identity documents at scale

This is one of the highest-ROI areas in financial services AI consulting. The data volumes are massive, the workflows are repetitive enough to benefit from automation, and the penalty exposure for failure is severe.

The Governance Imperative: Why Responsible AI Can't Be an Afterthought

Financial institutions face a governance environment that has gotten more demanding, not less. The EU AI Act classifies credit scoring and creditworthiness AI as high-risk. U.S. state-level AI legislation is expanding. The OCC, CFPB, and FCA are each scrutinizing model use - and regulators now treat documentation of data lineage, model validation records, and audit trails as baseline requirements.

This creates a specific challenge for AI consulting engagements.

What "Responsible AI" Actually Requires

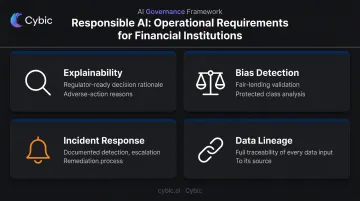

Responsible AI in financial services isn't a values statement - it's an operational checklist:

- Explainability: Can a regulator understand why a credit decision was made? Can you produce a specific adverse-action reason that satisfies CFPB requirements?

- Bias detection: Are protected classes being treated differently in ways the model can't justify? Has the model been validated against fair-lending standards?

- Incident response: What happens when a model produces an unexpected output? Is there a documented process for detection, escalation, and remediation?

- Data lineage: Can you trace every data input used in a decision back to its source?

These aren't optional. They're the minimum for a system that can survive regulatory review.

Governance by Design vs. Governance as Retrofit

Most AI projects in financial services fail at governance for the same reason: it gets treated as a review phase at the end, not a design principle at the beginning.

A team builds a capable model, deploys it, and then discovers the audit trail is inadequate, the access controls don't meet regulatory requirements, and the explainability layer is insufficient for adverse-action documentation. The remediation work is expensive and often requires rebuilding core components.

Building auditability, role-based access controls, and data governance into the system architecture from day one is less work overall - not more. You avoid spending months retrofitting controls onto a system that wasn't designed to accommodate them.

Cybic's approach embeds these controls at the architectural level: security, RBAC, encrypted data protection, and auditability of AI-driven actions are built in at the design stage - not added afterward. For financial services clients navigating requirements across multiple jurisdictions, this model is the difference between a system that clears regulatory review and one that gets shelved six months into deployment.

On data privacy specifically: financial institutions hold extraordinarily sensitive customer data. Cybic's policy is explicit - proprietary enterprise data is never used to train or fine-tune AI models. That commitment is enforced at the architectural level through access controls and audit trails, not just contractual language.

The Rise of Agentic AI in Financial Consulting

Agentic AI is qualitatively different from earlier automation. Earlier systems analyzed information and presented outputs for human review. Agentic systems act - executing transactions, initiating compliance alerts, routing cases, updating records - without waiting for a human to trigger each step.

McKinsey describes banks deploying autonomous agent squads for KYC and AML workflows, where agents handle case investigation, document retrieval, and escalation routing end-to-end. Banks currently allocate 10–15% of full-time equivalents to KYC/AML work while detecting approximately 2% of global financial crime flows - a ratio that makes the case for agentic automation on its own.

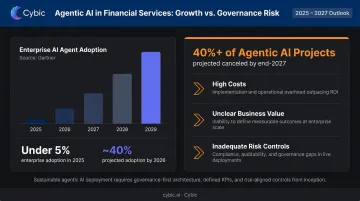

Gartner projects 40% of enterprise applications will include task-specific AI agents by 2026, up from less than 5% in 2025.

The Governance Questions Agentic AI Introduces

Autonomous action creates accountability questions that traditional AI governance frameworks weren't designed to address:

- Who is liable when an agent makes a consequential decision - the institution, the vendor, or both?

- What human-in-the-loop checkpoints are required before an agent can execute a transaction or close a case?

- What override protocols exist when an agent's decision needs to be challenged or reversed?

- How are agent actions logged to satisfy audit requirements?

Consultants helping financial institutions adopt agentic AI must define decision authority boundaries and escalation paths before deployment - not during the post-incident review.

The failure data reinforces that point. Gartner projects over 40% of agentic AI projects will be canceled by end-2027 due to costs, unclear business value, or inadequate risk controls. Organizations that deploy before their governance framework is in place account for a disproportionate share of those cancellations.

What Effective AI-Enabled Financial Services Consulting Actually Looks Like

The Execution Gap

Most financial institutions don't struggle to find AI consultants. They struggle to find partners who can bridge strategy and production deployment. KPMG found that even two years after the release of ChatGPT-3, financial services companies still struggled with transparency, explainability, data security, and integration into existing systems, with only 20% deeply integrating generative AI into operations.

An engagement that ends with a roadmap is an expensive planning exercise. The measure of effective AI consulting in financial services is working systems in production, not the quality of the presentation.

What Strong Delivery Actually Requires

Effective AI consulting in financial services is distinguished by a few specific capabilities:

- Engineering-led teams that build directly into existing infrastructure, not alongside it

- Legacy system integration into core banking platforms and data systems that weren't originally designed with AI in mind

- Compliance-first operation from day one, not after a governance review phase bolted on once the system is already built

Knowledge transfer is non-negotiable. Financial institutions that outsource AI development without building internal understanding create long-term dependency. The system becomes a black box that only the vendor can maintain, which is a fragile position under regulatory scrutiny.

What to Require of an AI Consulting Partner

Before engaging an AI consulting partner for a financial services project, institutions should verify:

- Pilot-to-production track record in regulated environments, with deployed systems to point to

- Demonstrated legacy system integration, not theoretical capability

- A delivery model that builds client capability rather than maximizing vendor dependency

That last requirement is where most engagements fall short. Cybic's engineering-led, infrastructure-agnostic delivery model is built around it specifically. Engagements are structured to deliver working systems, not recommendations, and to leave client teams more capable of operating and extending those systems on their own.

Frequently Asked Questions

How is AI used in the financial services industry?

AI is now embedded across fraud detection, credit risk modeling, KYC and AML compliance, customer service, regulatory reporting, and predictive analytics. It has evolved from narrow rule-based automation into core operational infrastructure that financial institutions depend on for both efficiency and regulatory compliance.

What is the difference between AI strategy consulting and AI implementation in financial services?

Strategy consulting delivers roadmaps and analysis; implementation consulting builds and deploys production-ready systems. Financial institutions need both capabilities in a single engagement. Organizations that separate the two typically end up with strategies that never get executed, or systems built without the strategic context to deliver real value.

How does AI improve regulatory compliance in financial services?

AI automates transaction monitoring, accelerates KYC document processing, improves accuracy in regulatory reporting, and generates audit trails at scale. One critical caveat: AI compliance tools must themselves meet regulatory standards for explainability and model documentation. A tool that creates new compliance exposure while solving an existing one is not a solution.

What are the biggest risks of deploying AI in financial services?

The primary risks are model bias (particularly in credit decisions affecting protected classes), data privacy exposure, lack of explainability creating regulatory non-compliance, and deploying systems that internal teams cannot adequately monitor or maintain. All four risks are reduced when governance is embedded at the architectural level rather than applied as an afterthought.

What is agentic AI, and how is it being used in financial services?

Agentic AI refers to systems that act autonomously rather than just analyze. In financial services, emerging use cases include intelligent KYC/AML case routing, autonomous compliance alert generation, and AI-driven advisory workflows. Governance frameworks for agentic systems are still maturing, which means accountability and oversight design must happen before deployment, not after.

How can financial institutions ensure their AI systems remain auditable?

Auditability requires designing systems with explainable model outputs, comprehensive audit logs, role-based access controls, and version control from the start. These controls work best when embedded at the architectural level. Retrofitting them onto existing systems costs more and rarely achieves the same coverage.