Introduction

Financial institutions process data at a scale that strains conventional AI architectures. Swift alone handles an average of 44 million FIN messages daily, while DTCC processes an average of $2.219 trillion in NSCC transactions every single day. Behind those numbers sits a fragmented market of 15 national securities exchanges and over 30 alternative trading systems - each generating pricing data, regulatory signals, and risk events that need simultaneous attention.

Most institutions responding to this complexity still rely on single-agent AI models - and that's where the architecture breaks down. A fraud classifier built for one task has no visibility into the compliance layer. A credit scoring model running in batch mode can't respond to intraday market shifts. The result: institutions collect isolated AI wins while continuing to run multi-step workflows manually across departments.

Multi-agent systems address this by assigning specialized roles to individual AI agents that operate in parallel across domains. This article covers what that architecture looks like across four layers, which ML strategies power it, what infrastructure it requires, and why governance must be built into the design - not added after the fact.

Key Takeaways

- Multi-agent systems run trading, fraud detection, risk monitoring, and compliance workflows in parallel - not sequentially.

- Core use cases: trading signal generation, fraud and AML detection, credit underwriting, portfolio research, and regulatory compliance.

- Four architectural layers: data perception → reasoning engine → strategy generation → execution and oversight.

- Governance over data access, agent permissions, and reasoning logic must be resolved before any technical build begins - gaps here are the most common cause of deployment failure.

Why Multi-Agent Systems Outperform Single-Agent AI in Finance

The Single-Agent Bottleneck

A single AI model handles one task well - a fraud classifier, an FAQ chatbot, a credit scoring model. None of these can coordinate with each other, share context across data types, or produce simultaneous outputs across departments.

Financial workflows don't work in isolation. A suspicious transaction needs to trigger both a fraud alert and a compliance review. A credit decision benefits from real-time economic indicators, not just a batch credit bureau pull from last week.

Single-agent architectures push these multi-step workflows back into human hands, or into sequential pipelines where each stage waits on the previous one.

Where Multi-Agent Design Changes the Equation

Multi-agent systems decompose complex workflows into specialized roles that run in parallel, not in sequence:

- A market data agent processes live price feeds and economic signals

- A compliance agent interprets regulatory filings and policy updates

- A behavioral agent monitors anomaly patterns across transactions

The result is faster, more contextually complete output than any single model could produce alone.

Research on multi-agent LLM architectures for financial compliance demonstrates this with document-processing experiments scaling from 1,000 to 100,000 documents per day - workloads that would overwhelm sequential single-agent pipelines.

That scalability advantage is real, but it comes with added architectural complexity. Multi-agent design isn't always the right call.

When Multi-Agent Is Not the Answer

Multi-agent architecture is not always justified. If the goal is narrow - summarizing a document, answering FAQs, running a simple classification - a RAG model or single agent is cheaper and easier to govern. Multi-agent systems earn their complexity when workflows:

- Cross organizational silos (trading desk + compliance + risk, simultaneously)

- Combine rule-based and market-driven logic

- Require parallel outputs from heterogeneous data types

- Demand coordination across execution, monitoring, and audit systems in real time

Key Applications of Multi-Agent AI in Financial Services

Autonomous Trading

In trading, multi-agent pipelines assign discrete roles: one agent synthesizes price signals, another interprets news and sentiment, a third handles macroeconomic context, and a fourth prepares order parameters. These run in parallel rather than in a serial chain.

The CFTC has documented that automated trading systems were present in over 60% of all futures volume - with nearly 80% of FX futures handled by automated systems. At that scale, latency in the signal pipeline is a competitive disadvantage.

Critically, the appropriate model here is bounded autonomy. The Knight Capital incident (a coding error that cost the firm over $460 million in a single day) is the clearest proof that fully autonomous trading agents without pre-trade limits, test environments, and human escalation gates create catastrophic tail risk.

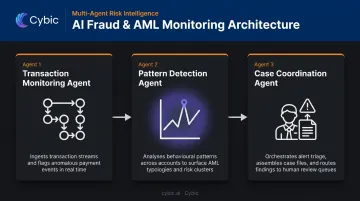

Fraud Detection and AML Monitoring

Multi-agent fraud architectures typically separate three functions:

- A transaction monitoring agent ingests raw payment flows continuously

- A pattern detection agent compares activity against behavioral baselines to flag anomalies

- A case coordination agent routes high-confidence alerts to human reviewers for final determination

Mastercard's implementation of generative AI for fraud detection boosted detection rates by 20% on average and up to 300% in specific cases. The advantage over static rule engines: these agents learn continuously, adapting to new fraud patterns rather than waiting for manual rule updates.

Credit Scoring and Loan Underwriting

Traditional credit scoring is point-in-time and bureau-dependent. That model leaves 7 million U.S. consumers effectively invisible to lenders - people with thin files who don't lack creditworthiness, just documentation.

Multi-agent underwriting changes this by running parallel assessments:

- One agent evaluates traditional financial history

- A second processes behavioral and alternative data signals

- A third integrates real-time economic indicators

Upstart's AI model, under CFPB review, approved 27% more borrowers than traditional models at 16% lower average APRs. Multi-perspective evaluation surfaces creditworthy borrowers that single-model scoring consistently misses.

Portfolio Management and Investment Research

In asset management, agents function as co-pilots, not autonomous allocators. Fiduciary obligations mean the final allocation decision stays with the human manager - but that doesn't make agents less valuable.

Mercer research across 150 asset managers found 55% had AI integrated in at least one investment process. Agents handle macro synthesis, investment memo generation, scenario analyses, and stress tests - compressing research that once took days into outputs reviewable in hours.

Deterministic workflows (rule-based, like insurance policy checks) and nondeterministic workflows (market-driven, like dynamic portfolio rebalancing) require different agent architectures. Compliance agents need tighter predetermined code paths; research agents benefit from the flexibility of LLM-directed agentic flows - a distinction LangGraph's framework captures directly.

Regulatory Compliance and KYC

UK financial institutions spent £38.3 billion on financial crime compliance in 2023 - up 32% since 2021. The TD Bank AML failure cost $450 million in civil penalties from the OCC alone. The financial and reputational cost of manual compliance gaps is documented and ongoing.

Compliance agents reduce this exposure by:

- Continuously monitoring transaction logs against regulatory thresholds

- Automating KYC screenings and cross-referencing entity databases

- Flagging regulatory anomalies in real time rather than through periodic audits

- Cross-referencing internal workflows against applicable regulations (GDPR, FINRA, AML directives)

Regulators are explicit that AI systems remain subject to existing oversight obligations, including FINRA Rule 3110 supervision. Compliance agents don't replace that oversight - they reduce the manual review burden on the 90% of routine cases, freeing human reviewers to focus on complex escalations.

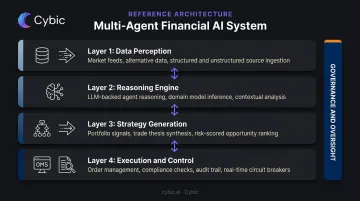

The Four-Layer Architecture of a Multi-Agent Financial AI System

Layer 1 - Data Perception

This layer handles ingestion from every relevant data source: real-time market feeds, SEC filings, earnings call transcripts, news, social sentiment, blockchain transaction data, and internal risk and compliance databases.

The engineering challenge here isn't just data volume. The harder problem is governance: which agents can access customer-level data vs. public market data, how timestamps are normalized across asynchronous feeds, and what audit trail exists for each data source used in a downstream decision. These questions need architectural answers before any ML model touches the data.

Layer 2 - Reasoning Engine

No single model type handles all financial reasoning tasks. The reasoning layer combines:

- Domain-tuned LLMs for interpreting unstructured text (earnings transcripts, regulatory filings, news)

- Retrieval systems for pulling historical context into current decisions

- Statistical forecasting models for return and volatility prediction

- Optimization modules for translating forecasts into feasible portfolio configurations

BloombergGPT, trained on a 363-billion token financial dataset with 50 billion parameters, illustrates the degree of domain specialization that financial NLP tasks actually require. General-purpose LLMs handle surface-level financial language adequately; the edge cases that matter in regulated environments need domain-specific grounding.

Layer 3 - Strategy Generation

This is where AI insight becomes economically actionable. The strategy generation layer converts analytical outputs into decision objects: structured representations of potential actions (trade proposals, risk alerts, rebalancing suggestions, compliance flags) along with the reasoning chain and institutional constraints that govern them.

This layer must reconcile forecasts against hard limits: portfolio mandates, liquidity constraints, regulatory caps, and counterparty exposure limits. An agent that generates a technically correct recommendation while violating an investment mandate creates direct compliance and legal exposure - not just an operational error.

Layer 4 - Execution and Control

The execution layer connects to the full financial infrastructure stack:

- OMS/EMS systems and exchange APIs

- Smart contracts and approval workflows

- Position limit frameworks, audit logs, and emergency stop mechanisms

Most production financial agents operate under bounded autonomy at this layer - generating recommendations within defined limits, escalating exceptions to human reviewers, and logging every action and intermediate reasoning step for audit reconstruction.

Five cross-cutting design dimensions determine how these layers interact:

| Dimension | What It Governs |

|---|---|

| Autonomy depth | How much an agent can act without human approval |

| Model heterogeneity | Diversity of models and data sources across agents |

| Execution coupling | How agents synchronize responses to shared signals |

| Infrastructure concentration | Reliance on common cloud providers or APIs |

| Supervisory observability | Ability to audit and reconstruct agent decision paths |

Infrastructure, Technology Stack, and Frameworks

Agent Orchestration

LangChain/LangGraph connects models, data sources, and tools into structured multi-agent workflows. LangGraph specifically enables the deterministic control flows that compliance-sensitive financial applications require.

CrewAI provides role-specialized crews where each agent has defined responsibilities and communication protocols, structured similarly to how a trading floor operates: distinct roles for signal generation, risk review, and execution.

AWS Bedrock and Azure OpenAI offer cloud-native deployment with data residency controls that matter for EU institutions operating under GDPR. Azure's stated policy - that customer prompts and completions are not used to train OpenAI models - is a material governance consideration for financial clients.

Data Pipeline Infrastructure

Real-time and batch pipelines serve different use cases and require different architectures:

- Real-time streaming pipelines: required for trading signal generation and fraud detection where latency is measured in milliseconds

- Batch pipelines: adequate for credit scoring, compliance reporting, and portfolio attribution

Financial data sources - market feeds, sentiment APIs, SEC EDGAR - need vector database integration for retrieval-augmented generation. Data pipeline governance determines what signals agents can act on and at what speed.

Compute Architecture

Training large ML models - deep neural networks and reinforcement learning models - requires high-performance GPU infrastructure. BloombergGPT's training required 512 NVIDIA A100 GPUs over 53 days - the high end of the range. Inference workloads are lighter, but still require GPU capacity for low-latency deployment.

Deployment trade-offs by environment:

- Cloud: Fast scaling, managed services, regional compliance configurations

- On-premises: Maximum data control, lowest latency for sensitive workloads

- Hybrid: Sensitive data on-premises, variable compute loads in cloud

Infrastructure-Agnostic Deployment

These deployment trade-offs compound over time. Financial institutions frequently need to shift data residency, add on-prem compute for sensitive workloads, or adopt a new cloud region as regulations change - and rebuilding infrastructure each time carries real cost. Systems that operate consistently across cloud, hybrid, and on-prem environments without governance trade-offs avoid that trap.

Cybic's Drava platform applies this directly: it connects enterprise data, ML models, AI reasoning, and intelligent agents in a unified architecture that runs across AWS, Azure, and Google Cloud with consistent governance controls - RBAC, encrypted data protection, and full workflow auditability - regardless of where workloads are deployed.

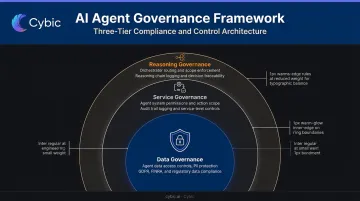

Governance, Security, and Compliance in Multi-Agent Finance Systems

Three-Layer Governance Architecture

Governance in multi-agent finance systems operates at three distinct levels - and all three must be defined before the first line of code is written:

Data governance: Which agents access which data fields, under what permission levels, and in compliance with GDPR, FINRA, and applicable banking regulations. Public market data and customer PII require completely different access controls.

Service governance: Which agents can trigger which systems, what actions they can perform, and what the full audit trail looks like for each action. An agent that can place trades and one that can only generate recommendations need fundamentally different permission scopes.

Reasoning governance: How the orchestrator routes tasks to sub-agents, how those agents stay within their defined scope, and how the reasoning chain is logged for compliance reconstruction.

FINRA's 2024 guidance is explicit: generative AI and LLM use remains subject to existing supervision obligations under Rule 3110. The Federal Reserve's SR 11-7 model risk management framework applies to AI models the same way it applies to traditional quantitative models. DORA adds ICT resilience obligations for EU-regulated entities. For regulated financial institutions, governance is the baseline requirement, not an architectural afterthought.

Security Threats Specific to Multi-Agent Systems

NIST AI 600-1 and OWASP's agentic AI threat taxonomy identify several attack vectors that are unique to multi-agent architectures:

- Memory poisoning: Injecting false data into agent memory to corrupt downstream decisions (loan approvals, risk assessments)

- Tool misuse via adversarial prompts: Manipulating an agent's tool-calling behavior through crafted inputs

- Identity spoofing between agents: One agent impersonating another to gain unauthorized capabilities

- Cascading hallucinations: Misinformation from one agent propagating through the system and compounding across subsequent reasoning steps

- Communication channel attacks: Intercepting or manipulating inter-agent message passing

Mitigations require architectural solutions: cryptographic input validation, role-based access control at the agent level, encrypted inter-agent communications, and human-in-the-loop gates for high-stakes decisions. BIS research notes that lack of AI explainability could contribute to systemic risk, which makes building supervisory observability into every layer a compliance requirement, not just a best practice.

Cybic builds these controls into the architecture from day one: role-based access control at the agent level, encrypted data protection in transit and at rest, full auditability of AI-driven workflows, and a firm policy against training models on proprietary enterprise data. In a regulated deployment, those aren't optional enhancements - they're the conditions under which a system can operate at all.

Frequently Asked Questions

What are the applications of AI in finance?

AI in finance covers a wide range of use cases, each suited to different model architectures:

- Trading and market analysis

- Fraud detection and AML monitoring

- Credit scoring and loan underwriting

- Portfolio management and research

- Regulatory compliance and KYC automation

- Customer-facing advisory tools

What is the architecture of a multi-agent system in AI?

Multi-agent systems follow four layers: data perception (ingesting heterogeneous inputs), reasoning engine (interpreting and forecasting), strategy generation (producing structured decision objects), and execution with control (connecting to operational systems with human oversight and audit trails). Governance controls span all four layers.

What are the applications of multi-agent systems in AI?

Multi-agent systems apply wherever tasks require parallel processing across specialized roles: finance, healthcare, supply chain, energy, and legal workflows. They enable end-to-end workflow automation that sequential single-model pipelines cannot achieve, especially when tasks cross organizational silos or combine outputs from multiple data types.

What are the top AI tools for finance?

Key tools by category:

- Orchestration: LangChain/LangGraph for agent workflow management

- LLM infrastructure: AWS Bedrock, Azure OpenAI

- Data ingestion: Bloomberg terminal APIs, yfinance, SEC EDGAR

- Financial NLP: BloombergGPT (50B parameters) or FinGPT (open-source alternative)

When should a financial institution use a multi-agent system instead of a single AI model?

Multi-agent systems are warranted when workflows cross multiple departments, combine rule-based and market-driven logic, or require simultaneous outputs from different data types. Single agents or RAG models are sufficient for narrow, isolated tasks like document summarization, FAQ responses, or simple classification.

How do you ensure compliance and security in multi-agent AI systems for finance?

Compliance requires governance embedded at the architectural level: data access controls, agent permission boundaries, encrypted communications, and human approval gates for high-stakes actions. Every AI-driven decision must be auditable and reconstructable, aligned with GDPR, FINRA Rule 3110, SR 11-7, and DORA for EU entities.