Introduction

Fintech builders face a structural contradiction. Investors push for 90-day pilots, market windows close fast, and competitors ship constantly - while regulators demand explainability, auditability, and bias controls baked into every automated decision. Most teams resolve this tension the wrong way: they move fast, skip governance, and hit a wall during security review or regulatory audit.

The result is predictable. Gartner predicts at least 30% of generative AI projects will be abandoned after proof of concept by end of 2025 - with inadequate risk controls and poor data quality cited as primary causes. In fintech, the stakes are higher. A demo that cannot explain its credit decisions or survive a compliance audit isn't a product - it's a liability.

Trusted AI solutions change this equation. When governance is embedded at the architectural level from day one rather than bolted on later, fintech teams move faster overall with fewer delays, not more.

Key Takeaways

- The right AI architecture delivers speed and regulatory trust at the same time - no trade-off required.

- Trusted AI builds explainability, auditability, and data governance into the architecture from day one.

- AI compresses timelines across every concept stage - ideation, prototyping, compliance mapping, and stakeholder validation.

- Governance-first AI eliminates the compliance rebuild cycle that kills most fintech timelines.

- Evaluate AI solutions on governance architecture, infrastructure flexibility, and engineering delivery, not demo quality.

The Speed-Trust Dilemma in Fintech Concept Development

The pressure is real on both sides. Venture timelines and first-mover dynamics push fintech teams toward rapid iteration. Regulators - SEC, FINRA, CFPB, FDIC - push back with explainability mandates, audit requirements, and fair lending standards that don't bend for speed.

Most teams end up in a "pilot trap": they build something fast, it impresses stakeholders, and then it stalls. Only 25% of enterprise organizations have moved 40% or more of their AI pilots into production, according to Deloitte's State of AI in the Enterprise. Speed without governance-readiness produces demos, not deployable products.

Why Fintech Concept Development Is Uniquely High-Stakes

In most industries, compliance can be retrofitted. In fintech, it cannot.

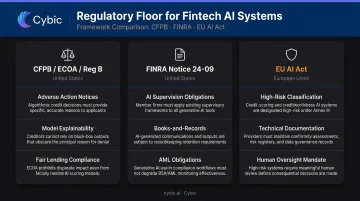

Three regulatory frameworks set the floor for any AI system in this space:

- CFPB (ECOA/Reg B): Creditors using complex algorithms must still provide specific and accurate adverse-action reasons. A credit limit decision needs a traceable rationale trail, not just a score.

- FINRA Notice 24-09: Broker-dealer use of generative AI remains subject to supervision, books-and-records, and AML obligations.

- EU AI Act: Creditworthiness evaluation systems are classified as high-risk AI, with corresponding documentation requirements.

Regulatory exposure is only part of the risk. The infrastructure underneath the model matters just as much. One in four banking executives cites unstructured data quality as a primary challenge to scaling AI, per McKinsey. AI built on fragmented data infrastructure produces models that fail in production - which means data fabric decisions made at the concept stage are architectural, not administrative.

The Governance Gap That Kills Fintech Concepts

Most rapid development tooling is optimized for flexibility, not financial compliance. Teams discover this gap late - during legal review, security audit, or regulatory examination - and face a binary choice: rebuild or abandon.

The SEC's 2024 enforcement actions against Delphia ($225,000 penalty) and Global Predictions ($175,000 penalty) illustrate the cost of AI claims that outpace underlying governance.

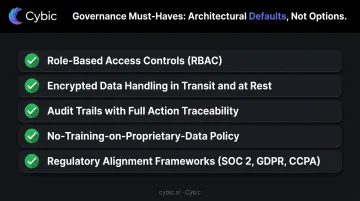

Trusted AI solutions close this gap differently. Role-based access controls, encrypted data handling, and audit-trail mechanisms are embedded at the architectural level, not layered on afterward.

For fintech specifically, this matters because proprietary financial data - transaction histories, credit profiles, behavioral data - cannot be exposed to external model training pipelines. That separation must be enforced by architecture, not policy.

What Trusted AI Solutions Actually Deliver in Fintech

"Trusted AI" gets used loosely. In fintech, it has a precise meaning.

The NIST AI Risk Management Framework defines trustworthy AI characteristics as valid and reliable, secure and resilient, accountable and transparent, explainable and interpretable, privacy-enhanced, and fair with managed bias. In a fintech production context, these translate into four non-negotiable properties.

The Four Pillars That Matter for Fintech Builders

1. Explainability Fintech AI systems must produce outputs that a regulator, compliance officer, or non-technical auditor can interpret. Black-box models that deliver accurate predictions but cannot justify their outputs are non-viable in consumer lending, insurance underwriting, or investment advisory. This isn't a preference - it's a legal requirement under ECOA and analogous frameworks.

2. Auditability and Traceability Every AI-driven action, decision, and workflow step must be logged and navigable. When a compliance officer asks "how did the system arrive at this outcome," there needs to be a complete record, not just a model version number.

That completeness is what separates production-grade fintech AI from prototype-grade AI. Prototypes can skip logging. Production systems cannot.

3. Data Governance with No Proprietary Training Leakage Fintech teams handle transaction histories, credit profiles, and behavioral data that cannot feed external model training pipelines. A trusted AI solution must enforce strict separation between operational enterprise data and model training processes. That separation needs to be architectural, not buried in terms of service language.

4. Compliance-by-Design Architecture Governance frameworks should be part of the system architecture from the first design decision. Cybic's approach reflects this directly: security controls, RBAC, auditability, and regulatory alignment are incorporated at the architectural level across every engagement - not configured after the build is complete.

Why Governance Embedded by Design Enables Faster Concept Development

Building governance in from the start feels like overhead. It isn't - it's the faster path when you account for total development time.

Traditional model risk management review adds six to twelve weeks of sequential review after development is complete, per McKinsey research. Teams that skip governance in early builds don't save that time - they borrow it. They pay it back later, with interest, during the rebuild cycle.

Cybic's Drava platform demonstrates this directly. It unifies enterprise data, ML and data science, AI reasoning, and intelligent agents under a single governed architecture, with RBAC, encrypted data protection, audit trails, and no-proprietary-data-training enforcement built in from the start. Fintech concepts built on this foundation reach internal review with compliance documentation already in place.

How AI Accelerates Every Stage of Fintech Concept Development

AI doesn't compress just one part of fintech concept development - it shortens timelines at every stage, when deployed by teams who understand financial domain constraints from the start.

From Ideation to Prototype

LLM-powered systems can synthesize regulatory landscape summaries, competitive positioning, and market gap analysis in hours rather than weeks. What previously required weeks of analyst research now serves as a rapid stress-test before any development investment is committed.

From there, AI solutions can ingest disparate data sources - transaction logs, market data, customer profiles - and model the data fabric a fintech product needs to function. The time between "what data do we need?" and "here is a working data model" collapses fast.

For fintech teams constrained by legacy infrastructure, this stage is where infrastructure-agnostic delivery matters most. Cybic builds across AWS, Azure, and Google Cloud, integrating into existing financial data systems rather than requiring parallel infrastructure.

AI-powered workflow orchestration allows fintech teams to build demo-ready prototypes that simulate real financial workflows - fraud detection logic, compliance monitoring, credit scoring pipelines - without full engineering builds. McKinsey's research on developer productivity with generative AI found coding task completion up to twice as fast, with code documentation improvements of 45–50%. The same productivity gains apply to prototype construction in financial services contexts.

From Prototype to Stakeholder-Ready

AI systems with embedded regulatory alignment can map a concept's data flows and decision points against AML requirements, fair lending rules, and data privacy mandates at the prototype stage - before significant development investment has been made. Discovering a GDPR gap at prototype costs a sprint. Discovering it post-build costs months.

Generative AI copilots embedded into the development workflow support product, legal, engineering, and compliance teams simultaneously - surfacing relevant precedents, flagging regulatory risks, and suggesting architecture adjustments.

Cybic builds enterprise GenAI copilots integrated via governed pipelines on AWS, Azure, and Google Cloud, designed specifically for this kind of cross-functional decision support.

How to Evaluate AI Solutions for Fintech Concept Development

Not all AI solutions are viable for fintech. Here's what to evaluate specifically.

Governance and Compliance Architecture

Ask whether the AI solution has security controls, auditability, and regulatory alignment built into the architecture itself - not as optional add-ons.

Non-negotiable features:

- Role-based access controls (RBAC)

- Encrypted data handling in transit and at rest

- Audit trails with full action traceability

- Strict no-training-on-proprietary-data policy

- Regulatory alignment frameworks for relevant standards (SOC 2, GDPR, CCPA)

If any of these are configuration options rather than architectural defaults, they will get missed under time pressure.

Infrastructure Flexibility and Integration Depth

A fintech organization with ten years of legacy data infrastructure cannot rebuild it for a new AI system. Evaluate whether the AI solution operates across existing infrastructure - cloud, hybrid, or on-prem - without requiring ecosystem migration.

Cybic's infrastructure-agnostic model is built for this constraint. It operates across AWS, Azure, Google Cloud, Snowflake, and Databricks, with legacy modernization services that maintain operational continuity while progressively integrating AI into existing financial data systems.

Engineering-Led Delivery vs. Demo Culture

Infrastructure fit is only half the equation. How a vendor delivers - and what they actually hand off - matters just as much. A sophisticated demonstration is not a production-ready system.

When evaluating vendors, ask three questions:

- What specifically gets delivered at the end of this engagement?

- How does it integrate into our existing stack?

- What is the documented path from prototype to production?

Vendors who cannot answer these concretely are selling presentations. Cybic structures every engagement around a working, integrated system at the end - not a report or a roadmap. Engineers architect, build, and deploy directly, which closes the gap between what gets designed and what actually runs in production.

Frequently Asked Questions

What are the AI solutions for fintech?

AI solutions for fintech include ML platforms for credit scoring and fraud detection, generative AI and LLM applications for compliance automation and customer engagement, intelligent workflow automation, and governed data platforms. The most impactful solutions embed governance and compliance into the architecture rather than treating them as separate controls.

What is an AI fintech developer?

An AI fintech developer is an engineering team or company that designs and builds AI-powered financial technology systems - covering model development, LLM applications, intelligent automation, and data infrastructure - with specialized knowledge of financial domain requirements including regulatory compliance, auditability, and data security.

What does "trusted AI" mean in fintech development?

Trusted AI in fintech means systems that are explainable, secure, and compliant by design - where decisions can be audited, data is encrypted and never used for external model training, and regulatory requirements are embedded in the architecture. This stands in contrast to black-box models that regulators and risk teams cannot scrutinize.

How does AI speed up fintech concept development?

AI compresses timelines at every stage: market analysis and ideation, data modeling, prototype generation, compliance gap identification, and stakeholder validation. The biggest gains come from AI that incorporates compliance considerations from the earliest concept stages, avoiding the rebuild cycles that erase time saved downstream.

What governance features should AI solutions for fintech include?

Essential governance features include role-based access controls, full audit trails, encrypted data handling in transit and at rest, strict separation between enterprise data and model training pipelines, and regulatory alignment frameworks. These must be architectural defaults, not optional configurations that get skipped under delivery pressure.