Introduction

US banks process millions of sensitive customer records every day - Social Security numbers, transaction histories, account balances, credit profiles. One governance failure can set off a cascade: regulatory fines, fraud losses, audit failures, and the kind of reputational damage that takes years to repair.

The numbers make this concrete. US regulators issued nearly 50 fines in 2024, with North America accounting for 95% of global enforcement actions totaling $4.6 billion. Transaction-monitoring breaches alone rose 100% year over year. TD Bank paid over $1.3 billion to FinCEN for BSA violations. Citibank absorbed a $75 million OCC penalty specifically tied to data governance and data quality failures.

Penalties at this scale reflect a structural problem: banks that treat data governance as a compliance checkbox rather than an operational discipline keep paying for it.

This guide covers what data governance actually means in banking, which regulations are driving its requirements, how to build a functional framework, and where AI is changing how compliance gets done.

Key Takeaways

- Data governance in banking is the structured system of policies, roles, and controls that ensures financial data is accurate, secure, compliant, and accessible throughout its lifecycle.

- US banks must navigate BSA/AML, Dodd-Frank, GLBA, BCBS 239, GDPR, and CCPA - often with overlapping and conflicting requirements.

- Effective frameworks define roles, enforce data quality standards, track lineage, control access, and manage lifecycle policies.

- Legacy systems, data silos, and cultural resistance most commonly stall implementation.

- AI is shifting governance from periodic audits to continuous, automated compliance enforcement.

What Is Data Governance in Banking?

Data governance in banking is the structured system of policies, processes, roles, and technologies that defines how data is collected, stored, accessed, protected, and used. What distinguishes it from governance in other industries is the weight of regulatory obligation and fiduciary responsibility attached to every data decision.

It applies across all data types a bank handles: customer PII, transaction records, market data, loan documentation, internal communications, and increasingly, the outputs generated by AI models used in credit decisioning or fraud detection. That scope - and the accountability gaps it creates - is exactly why the distinction between governance and data management matters.

Governance vs. Data Management

These terms get conflated constantly, and the confusion creates real compliance gaps.

- Data governance defines the rules - who owns which data, who can access it, under what conditions, and who is accountable when something goes wrong.

- Data management is the operational execution of those rules - the pipelines, storage systems, quality checks, and tools that make governance real.

Governance without management is documentation. Management without governance is infrastructure with no accountability structure. In banking, both must be tightly integrated and continuously enforced.

The Financial Case

Gartner estimates that poor data quality costs organizations an average of $12.9 million per year. In banking, the consequences extend further: regulatory penalties, loan decision errors, inaccurate capital ratio calculations, and failed audits.

Two recent examples illustrate the scale:

- Citibank received a $75 million OCC penalty in 2024 for persistent data quality and governance weaknesses in regulatory reporting.

- JPMorgan Chase absorbed roughly $348 million in combined Fed and OCC penalties for inadequate trading activity monitoring.

These aren't edge cases. They're the predictable cost of treating governance as a back-office formality.

Key Compliance Regulations Banks Must Navigate

US banks don't operate under one regulation - they operate under a stack of overlapping federal and state requirements, each with distinct data obligations. Non-compliance consequences extend beyond fines to consent orders, operational restrictions, and credit rating impacts.

Dodd-Frank and BSA/AML Requirements

Dodd-Frank imposes significant data reporting requirements. Stress testing under the FR Y-14 collection framework applies to holding companies with $100 billion or more in total consolidated assets, demanding clean, consistently formatted, traceable data that can withstand Fed scrutiny.

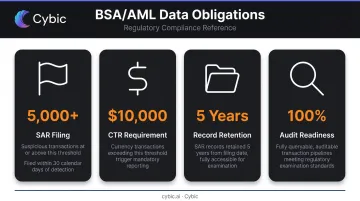

BSA/AML requirements are more operationally intensive:

- SARs must be filed for suspicious transactions involving $5,000 or more, within 30 calendar days of detection

- CTRs are required for currency transactions exceeding $10,000

- SAR records must be retained for five years from filing

- Banks must maintain queryable, fully auditable transaction pipelines to support FinCEN examinations

TD Bank's $1.3 billion FinCEN penalty in 2024 traced directly to SAR failures, AML program breakdowns, and transaction-monitoring backlogs - all data governance failures at their core.

GDPR and CCPA for Customer Data

GDPR applies to any US bank that holds or processes data belonging to EU residents - regardless of where the bank is headquartered. Key requirements:

- Breach notification to the supervisory authority within 72 hours of awareness

- Right to erasure (Article 17) for data subjects under specified conditions

- Consent management and documented legal basis for processing

CCPA covers California residents and grants rights to know, delete, correct, opt out of data sharing, and limit use of sensitive personal information. Note that CCPA's GLBA exemption applies to most bank customer data, but the security breach liability provision (Section 1798.150) still applies.

Both regulations require banks to know exactly what data they hold, where it lives, and who can access it. Data cataloging and classification are the operational foundation that makes both obligations achievable.

BCBS 239 and Basel III Risk Reporting

BCBS 239's 14 principles govern risk data aggregation and reporting for systemically important banks. The framework requires:

- Integrated data taxonomies, metadata management, and unified naming conventions (Principle 2)

- Accurate, largely automated risk data aggregation to minimize manual error (Principle 3)

- Capture of all material risk data across the full banking group (Principle 4)

Despite being published over a decade ago, BIS reported in 2023 that significant implementation work remains at most banks. For banks still working through implementation, that gap represents active supervisory exposure, not a historical footnote.

BCBS 239 compliance also affects capital calculations directly. Basel III capital ratios - expressed as percentages of risk-weighted assets - require accurate underlying data at every input stage. Miscalculated inputs produce miscalculated ratios, with serious regulatory consequences.

Gramm-Leach-Bliley Act (GLBA) Safeguards Rule

GLBA's Safeguards Rule requires financial institutions to implement a comprehensive information security program. The FTC updated it in 2023, adding specific technical requirements that pushed many banks to revisit existing controls. Current requirements include:

- Access controls and inventory/classification of data and devices

- Encryption of customer information in transit and at rest

- Multi-factor authentication

- Logging and monitoring

- Written incident response plans

- Breach notification to the FTC within 30 days of discovering unauthorized access affecting 500 or more consumers

The Safeguards Rule sits at the intersection of data governance and information security. Gaps in data classification or access controls create direct Safeguards Rule exposure - and vice versa.

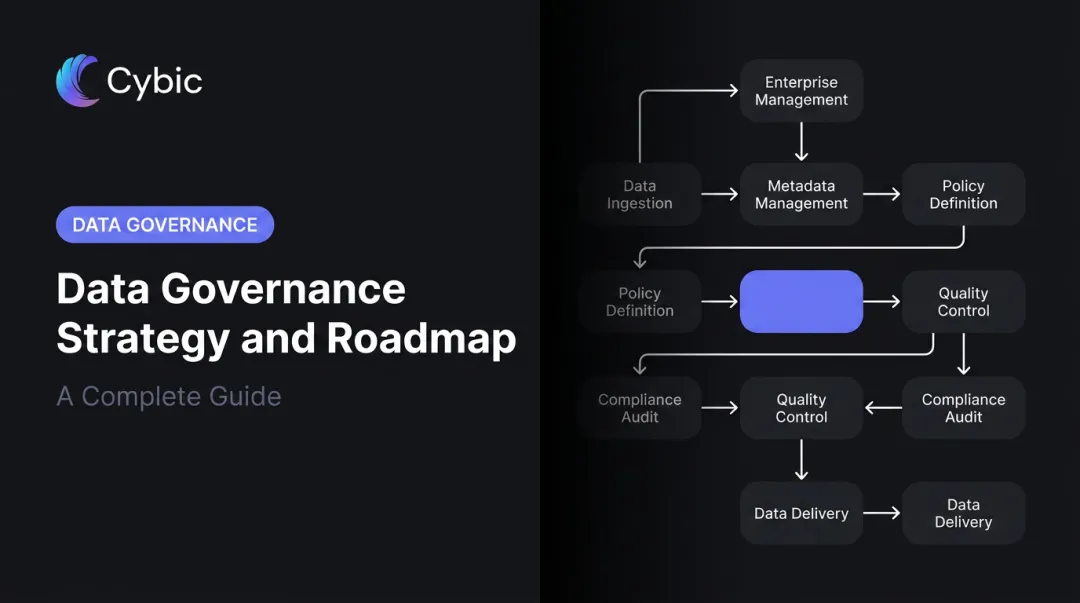

How to Build a Data Governance Framework for Banks

A banking data governance framework must align organizational accountability, data quality standards, access controls, and lifecycle policies to both business objectives and the full regulatory stack. Here's what a functional framework looks like in practice.

Define Roles and Accountability

Governance without named owners is unenforceable. Every data asset needs a person accountable for it.

| Role | Responsibility |

|---|---|

| Chief Data Officer (CDO) | Owns data strategy, policy, and cross-functional governance |

| Data Owners | Accountable for specific domains (credit, lending, customer) |

| Data Stewards | Day-to-day quality enforcement within domains |

| Data Custodians | Technical infrastructure - storage, access systems |

| Data Compliance Officers | Regulatory adherence and audit readiness |

This isn't an organizational chart exercise. Assigning these roles creates the accountability structures that make governance enforceable under examination.

Establish Data Quality Standards and Lineage

IBM identifies six core data quality dimensions that banking frameworks must enforce:

- Accuracy - data reflects the real-world entity it represents

- Completeness - no required fields missing

- Consistency - uniform format and definition across systems

- Timeliness - data available when needed for decisions and reporting

- Validity - data conforms to defined formats and rules

- Uniqueness - no unintended duplication of records

Data lineage - the traceable path from source to downstream use - ties these dimensions together in practice. BCBS 239's metadata and architecture requirements, BSA/AML audit trail obligations, and AI model validation all depend on it.

A business glossary with consistent definitions across departments prevents the "two departments, two definitions" problem that routinely surfaces in regulatory examinations.

Implement Access Controls and Lifecycle Management

Role-based access controls (RBAC) enforce the principle of least privilege: employees access only the data their role requires. Beyond security, RBAC is a governance control - it limits the scope of insider threats and reduces unauthorized data exposure across the organization.

Lifecycle management governs what happens to data over time:

- BSA requires five-year SAR and CTR record retention

- Archiving policies keep queryable data available for audits without cluttering operational systems

- Secure disposal procedures prevent regulated data from persisting beyond its required retention window

Platforms that embed RBAC and audit logging at the architecture level perform better in regulated environments than those that add compliance controls after deployment. Cybic's Drava platform is built on this governance-by-design principle - encrypted data protection, built-in RBAC, and full auditability of AI-driven actions are part of the architecture, not bolt-on features.

Technology Selection at Scale

Banks running on Snowflake, Databricks, or Azure need governance tools that integrate natively into those environments. Key selection criteria:

- Infrastructure-agnostic - supports cloud, hybrid, and on-premises

- Native integration with existing data platforms (no parallel shadow systems)

- Automated data catalog with classification and lineage tracking

- Immutable audit logging that satisfies regulatory examination requirements

Data Governance Best Practices in Banking

Shift from Reactive to Proactive Governance

Reactive governance - fixing problems after audits flag them - is expensive and creates recurring compliance risk. Every remediation cycle costs time, money, and regulatory goodwill.

Proactive governance uses automated data quality monitoring, anomaly detection, and continuous validation to surface issues before they escalate. This is particularly valuable for transaction data, where a pipeline degradation that goes undetected for even a week can create material SAR reporting gaps.

Treat Data as a Strategic Asset

Banks with mature governance frameworks don't just avoid penalties - they generate measurable business value from their data. Trusted, consistent data enables:

- Real-time fraud detection and AML monitoring

- Accurate credit risk scoring

- Customer 360 views for relationship management

- AI model training with defensible data provenance

Accenture's research found that digitally focused banks had market valuations 27% higher than less digitized peers and significantly better operating income per dollar of assets. That performance advantage starts with trusted, well-governed data - not just better technology.

Adopt a Federated Governance Model

Neither full centralization nor full decentralization works at scale in banking. Centralization slows execution; decentralization introduces inconsistency and regulatory gaps. Most mature banks land on a hybrid model:

- A central Data Management Office (DMO) led by the CDO sets enterprise-wide standards and regulatory baselines

- A cross-functional Data Council makes strategic decisions on data policy and investment

- Domain data owners and stewards execute within those guardrails for their specific business areas

This preserves domain expertise and operational speed while maintaining the consistency and accountability that regulators expect.

Automate Policy Enforcement

Manual compliance review cannot scale across thousands of data assets and constantly evolving regulatory requirements. At enterprise scale, manual review alone guarantees coverage gaps.

Automation addresses this through:

- Data quality rules engines that validate data in real time

- Automated sensitivity classification for PII and regulated data

- Access policy enforcement triggered by role changes

- Immutable audit logs that document every data action

Common Challenges in Banking Data Governance

Legacy Systems and Data Silos

Many US banks operate on core banking systems built decades ago - systems that were never designed for modern governance. The result is fragmented data, inconsistent schemas, and no native lineage tracking.

McKinsey found that one mid-sized bank spent two-thirds of its entire digitization budget on legacy systems - leaving little capacity for governance investment. M&A compounds the problem: merged institutions often inherit multiple disconnected data environments with conflicting definitions and duplicate records.

A data virtualization layer lets banks enforce governance policies across disparate systems without the cost and operational risk of full system replacement.

Multi-Jurisdictional Regulatory Complexity

Banks operating across states or internationally face overlapping, sometimes conflicting data regulations. Building separate compliance programs for each jurisdiction creates duplication, gaps, and audit complexity.

A more defensible approach has two parts:

- Centralized baseline policy: Calibrate to the most stringent applicable standard, then document jurisdiction-specific adjustments on top

- Regulatory change monitoring: Build a process so that when requirements shift - as they did with the 2023 GLBA Safeguards Rule update - the framework adapts systematically rather than reactively

Cultural Resistance and Change Management

Most governance programs fail because employees treat governance as bureaucratic overhead - something imposed on their work rather than something that makes their work faster, cleaner, and more defensible. Without executive sponsorship, governance initiatives stall in committee.

Practical tactics that actually work:

- Embed governance requirements into existing workflows - don't create parallel processes

- Provide role-specific training (what a data steward does vs. what a data owner does)

- Communicate metrics that show how governance improvements benefit individual teams, not just the compliance department

- Identify and empower governance champions at the business-unit level

AI, Automation, and the Future of Banking Data Governance

AI Transforming Governance Operations

Two-thirds of banks and insurers now use AI or machine learning techniques, with small-bank adoption jumping from 22% in 2023 to 52% in 2025. AI is changing what governance operations look like in practice:

- Classifies sensitive data at scale across millions of records automatically - a task manual processes cannot realistically perform

- Detects data quality degradation in pipelines before it creates compliance risk downstream

- Supports SAR automation and model documentation drafting through generative AI, cutting manual compliance workload

This shifts governance from a periodic audit function to continuous, near-real-time oversight. Cybic's Drava platform embeds auditability and traceability directly into the architecture, so banks can run AI-driven compliance workflows while keeping a defensible record for regulators.

Governing AI Itself

That continuous oversight extends to AI systems themselves. As banks deploy AI for credit decisioning, fraud detection, and customer communications, regulators are tightening scrutiny.

The CFPB's Circular 2022-03 makes clear that ECOA and Regulation B require specific adverse action reasons even when complex algorithms drive the decision - "the algorithm said so" is not a compliant explanation.

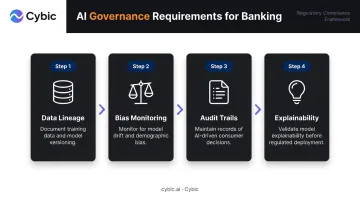

Banks must extend their governance frameworks to cover AI models specifically:

- Document training data lineage and model versioning

- Monitor for model drift and demographic bias

- Maintain audit trails of AI-driven decisions that affect consumers

- Validate model explainability before deployment in regulated workflows

Looking Ahead

Several emerging developments will reshape banking data governance over the next few years:

- Blockchain-based audit trails for payment and transaction data, reducing single-point-of-failure risk in recordkeeping

- Data ethics frameworks addressing algorithmic fairness in lending decisions

- Expanded federal AI oversight - current OCC model risk guidance acknowledges generative AI as novel and outside its current scope, but that gap won't persist indefinitely

Banks that build adaptive governance frameworks now, ones designed to absorb new data types, AI capabilities, and regulatory requirements without rebuilding from scratch, will be in a materially stronger position when these changes arrive. The cost of proactive architecture is almost always lower than the cost of reactive remediation.

Frequently Asked Questions

What is data governance in banking?

Data governance in banking is the structured system of policies, roles, and technologies that ensures financial data is accurate, secure, compliant, and accessible throughout its lifecycle. It defines accountability for every data asset and governs how data is collected, used, protected, and retired - with particular weight given to regulatory obligations and fiduciary responsibilities unique to financial institutions.

What regulations require data governance in US banks?

The primary frameworks are BSA/AML (transaction recordkeeping and SAR filing), Dodd-Frank (stress-test reporting), GLBA Safeguards Rule (information security), and BCBS 239 (risk data aggregation for systemically important banks). Banks holding EU resident data also face GDPR obligations; CCPA applies for California customers, with GLBA exemptions covering most records but not breach liability.

What are the key roles in a bank's data governance program?

Five roles are essential: Chief Data Officer (strategy), Data Owners (domain accountability), Data Stewards (quality enforcement), Data Custodians (infrastructure), and Data Compliance Officers (regulatory readiness). Every data asset must have a named owner - governance without that accountability structure is unenforceable.

What is the difference between data management and data governance in banking?

Data governance defines the rules, decision rights, and accountability structures - who can do what with which data and under what conditions. Data management is the operational execution of those rules through pipelines, systems, and tooling. Without governance, data management operates without enforceable standards; without management, governance policies exist only on paper.

How does data governance support fraud detection and risk management?

Fraud detection and AML monitoring depend on the quality of underlying data. Trusted, timely transaction data enables real-time anomaly detection and defensible SAR filing - while inaccurate data produces false positives, missed suspicious activity, and audit failures. Governance ensures the reliability and auditability these systems require to function correctly.

What are the biggest challenges in implementing data governance in banking?

The three most consistent obstacles are:

- Legacy systems that create data silos with no native lineage tracking

- Multi-jurisdictional complexity requiring simultaneous compliance with overlapping rules

- Cultural resistance that stalls adoption without executive sponsorship

All three require phased implementation, clear top-level accountability, and automation to scale what manual processes cannot.