Introduction

Banks are among the heaviest AI investors on the planet. According to IDC, the banking industry invested approximately $31.3 billion in AI in 2024 alone - the top AI-spending industry in both the Americas and EMEA. Yet despite that capital, MIT NANDA's 2025 research found that 95% of enterprise GenAI pilots fail to generate sufficient business value, with only 5% reaching production scale.

In banking, the odds are worse. Regulatory complexity, risk-averse culture, and fragmented operating models create failure conditions that don't exist in other industries.

The barrier is rarely the model. A technically excellent fraud detection AI can sit unused because of organizational failures that have nothing to do with the technology:

- Compliance wasn't looped in until week 14

- Middle managers had no tools or mandate to drive adoption

- The underlying workflow was never redesigned for AI-generated outputs

This guide covers what you need to move from pilot to production:

- Why banking AI programs stall

- The four organizational pillars that determine whether AI scales

- A practical deployment roadmap

- A stakeholder engagement strategy

- The metrics that actually reflect business impact

Key Takeaways

- 95% of enterprise GenAI pilots fail - in banking, regulatory friction and risk-averse culture compound this further

- AI fails when organizational inertia, fragmented ownership, and misaligned incentives go unaddressed

- Four pillars drive AI-ready banks: executive alignment, process redesign, workforce enablement, and embedded governance

- Compliance and governance must be designed in from day one - not reviewed at the end

- Measure adoption depth and workflow utilization, not login rates or training completions

Why AI Change Management in Banking Isn't Like Any Other Tech Rollout

Rolling out a CRM or a cloud migration is disruptive. Rolling out AI in a bank is something different entirely.

Three structural factors make AI uniquely hard to absorb:

- AI produces probabilistic outputs. Unlike an ERP that returns deterministic results, AI recommendations come with confidence scores and edge cases. For compliance-trained staff accustomed to clear rules and audit trails, this creates rational distrust - not irrational resistance.

- AI replicates human judgment, not just process execution. A credit analyst's career capital is built on judgment. When an AI system produces credit memos or flags AML anomalies faster than any human can, it threatens professional identity - not just workflow. Most change programs never address this directly, which is why quiet resistance persists.

- Resistance degrades the model. Unlike legacy systems that simply run at reduced capacity when avoided, AI improves with usage. Teams that route around the AI tool are actively making it worse - compounding the adoption failure over time.

The Regulatory Amplifier

Banking operates under compliance scrutiny that has no equivalent in retail or manufacturing. SR 11-7 model risk management guidance requires documented development, validation, governance, and ongoing controls for every model.

CFPB Circular 2022-03 makes clear that ECOA adverse action notice requirements apply to AI-driven credit decisions regardless of model complexity. Fair lending, AML, and explainability obligations turn every AI deployment into a governance event.

Staff hesitation in this context isn't irrational. It reflects genuine personal accountability risk. A loan officer who accepts an AI recommendation that later draws a fair lending inquiry has real exposure - and they know it.

The Compliance Engagement Problem

In most bank AI programs, compliance and legal teams are engaged near the end of the deployment cycle - positioned as gatekeepers rather than co-designers. This pattern reliably creates bottlenecks, late-stage redesigns, and delayed launches.

The organizations that scale AI fastest seat their Chief Compliance Officer and risk leadership on the AI steering committee from day one - with both veto authority and a clear mandate to drive workable solutions alongside the technical team.

Why Bank AI Programs Get Stuck in Pilot Purgatory

BCG research shows that roughly three-quarters of financial institutions are still experimenting with GenAI, and fewer than 10% have measurable use cases in operation. The bottleneck is structural, not technical.

The Three Culprits

Pilots succeed in controlled conditions - clean data, cooperative teams, limited scope. Enterprise banking operations look nothing like that. Three specific failure modes explain the gap:

- Operating model inertia: AI recommendations still require manual compliance sign-off, erasing the time savings the model was supposed to deliver. The AI runs; the workflow doesn't change.

- Siloed ownership: No single business leader owns the AI outcome across risk, operations, and front-office functions. When something stalls, accountability diffuses - and nothing moves.

- Misaligned incentives: Performance KPIs - call volume, transaction throughput, ticket closure rates - remain unchanged even as AI changes how value is created. Staff are rewarded for old behaviors, not new ones.

The Middle Management Gap

Middle managers carry the heaviest change burden in any bank AI program. They must deliver existing results while managing a disruptive transition, absorbing pressure from executive sponsors above while fielding skepticism from their teams below.

McKinsey research found that middle managers currently spend less than 30% of their time on people leadership - the rest goes to administrative and individual-contributor work. They're already stretched.

Most banks over-invest in executive communications and frontline training, then leave middle management without the tools, authority, or air cover to actually drive adoption on the ground.

The Cost of Stalling

When these failure modes compound - inertia, diffused ownership, unsupported managers - the cost extends well beyond missed ROI. Prosci research shows 73% of employees impacted by organizational change experience moderate to high stress, and 54% of change-fatigued employees actively look for new roles. Teams that survived one failed AI rollout carry scar tissue into the next. Resistance compounds - and the organization's tolerance for AI-driven change shrinks with every stalled program.

The Four Pillars of an AI-Ready Banking Organization

Leadership Alignment and Visible Executive Sponsorship

A CEO endorsing the AI strategy in an all-hands is not alignment. Real alignment means the CFO, COO, Chief Risk Officer, and Chief Compliance Officer share a consistent narrative about what AI will and won't do, which risks they personally own, and how their functions will be measured differently.

Inconsistency at that level creates political cover for resistors. When the CRO signals skepticism in a steering meeting while the COO signals urgency, middle managers read the room and hedge toward inaction.

Deloitte's research found that twice as many financial-services laggards as leaders cited lack of executive commitment as a significant AI implementation barrier. The gap between pioneers and followers isn't technology - it's sponsorship depth.

One structural fix: tie AI outcomes to business-line performance, not to the analytics or innovation function. When a business leader's P&L reflects AI-driven revenue growth or risk reduction, the adoption conversation changes.

Process Redesign Around AI Capabilities

Bolting AI onto legacy workflows produces limited results. If the process still requires humans to manually replicate what the AI just did - reviewing the same data, restating the same conclusions - the transformation hasn't happened.

Consider fraud review. A manual investigation process designed for a team of 20 analysts reviewing 200 cases per day collapses when AI flags 2,000 cases per day. Analysts drown in volume, productivity falls, and leadership blames the model. The model isn't the problem. The escalation and exception-handling workflow was never redesigned to accommodate AI throughput.

BCG applies a 10-20-70 framework to banking AI programs: roughly 70% of AI impact comes from people and processes, not technology. The banks that scale AI fastest treat workflow redesign as equal in priority to model quality.

Core workflows that typically require redesign:

- Fraud alert triage and escalation

- AML transaction monitoring and case resolution

- Credit memo drafting and underwriting approval

- Customer onboarding identity verification

- Regulatory reporting compilation

Workforce Enablement and Role Redefinition

Workforce enablement in banking must go beyond tool training. Relationship managers, risk officers, and compliance staff need to understand how to interpret probabilistic AI outputs, when an override is warranted, and how personal accountability shifts when AI is involved in a regulated decision.

Three competencies matter most:

- Interpreting probabilistic model outputs without treating them as binary verdicts

- Knowing when to override AI recommendations and documenting the rationale

- Understanding personal liability boundaries under regulated AI-assisted decisions

The role redefinition framing is equally important. A teller freed from routine query resolution can focus on complex customer needs. An analyst freed from data compilation can focus on judgment and client advice. That career-positive narrative isn't just motivational language. It's an accurate description of where AI creates the most value, and stating it directly addresses the identity threat that drives quiet resistance.

Embedded Governance and Compliance Integration

In banking, AI governance isn't a post-deployment audit. It's an architectural requirement. Model explainability, fair lending compliance, auditability of AI-driven decisions, and data lineage must be built into the system design, not reviewed after the fact.

When governance is retrofitted, the sequence is predictable: compliance raises issues in final review, the project stalls for redesign, momentum collapses, and staff conclude that AI programs never actually ship. This pattern kills adoption before it starts.

Engineering partners who treat governance as a design constraint, rather than a deployment checklist, avoid this cycle entirely. Cybic builds security controls, role-based access, auditability, decision traceability, and regulatory alignment into the architecture from day one. Banks that work this way sidestep the late-stage redesign bottlenecks described above and build the foundational trust staff need to adopt AI-driven workflows with confidence.

A Practical AI Change Management Roadmap for Banks

Phase 1: Organizational Diagnostic (Weeks 1–8)

A banking-specific change readiness assessment isn't a generic survey. It's a structured mapping exercise across compliance, risk, operations, and front-office functions that answers three questions:

- Who are the influential stakeholders in each function, and where do they currently stand on AI adoption?

- Where is AI experimentation already happening - sanctioned or otherwise - and what can be learned from it?

- Where has pilot fatigue or active resistance already formed, and what caused it?

The output is a stakeholder map that directs change investment toward the highest-leverage pockets first - actionable intelligence, not a readiness score filed away after a steering committee review.

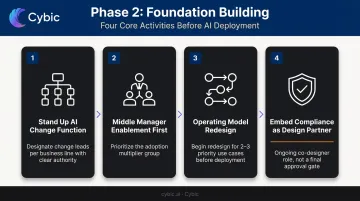

Phase 2: Foundation Building (Months 3–6)

The foundation phase sets the conditions for deployment. Key activities:

- Stand up a formal AI change function - or designate internal change leads in each business line with clear authority and support

- Prioritize middle manager enablement first - they are the adoption multiplier and the most under-supported group

- Begin operating model redesign for two or three priority use cases - don't wait for deployment to start this work

- Embed compliance review into the change architecture as an ongoing design partner, not a final approval gate

Phase 3: Wave Deployment and Institutional Scaling (Months 6–18)

Wave-based deployment starts with the business units that showed the highest readiness and the strongest operating model alignment in the diagnostic. Each wave is a learning event - friction points are documented, early wins are captured as internal case studies, and playbooks are updated before expanding.

That scaling pressure is where architecture decisions made early either pay off or create drag. Cybic's engineering-led delivery model is structured for this phase: solutions are built to integrate into existing infrastructure, compliance requirements, and team workflows from day one, which reduces both technical and governance risk as deployment scope grows.

Change management doesn't end when the last wave ships. It becomes a permanent institutional function with ongoing responsibilities:

- Monitoring adoption depth across business lines

- Updating training as workflows and AI capabilities evolve

- Managing organizational response as new use cases are introduced

Getting Stakeholder Buy-In: From Tellers to the C-Suite

The stakeholder challenge in banking is layered. C-suite sponsors set strategy but are distant from daily friction. Middle managers feel the operational squeeze most acutely. Frontline staff - tellers, call center agents, loan officers - are the actual adopters whose daily behavior determines whether AI activates or stalls.

Each layer requires a different engagement strategy:

- C-suite: Regular reporting on adoption depth and net value realized - not technology updates. Connect AI outcomes to business-line KPIs they already own.

- Middle managers: Give them tools, decision rights, and visible support. They need to answer their teams' questions and escalate friction points without feeling exposed.

- Frontline staff (co-design): Involve frontline employees in shaping chatbot escalation scripts and workflow adjustments. Co-design creates ownership and surfaces practical issues before deployment, not after.

- Frontline staff (training): Role-specific micro-learning tied to real scenarios - interpreting an AI fraud flag, deciding when to override a credit recommendation - builds confidence faster than generic compliance training.

Change Champions as the Connective Tissue

A distributed network of change champions embedded in each business unit is the most effective adoption infrastructure in a banking environment. Select them based on peer trust and credibility, not seniority.

Effective champions do three things their counterparts in formal leadership cannot:

- Translate the AI narrative into daily workflow language their teams actually use

- Surface quiet resistance before it hardens into structural opposition

- Provide peer credibility that top-down mandates cannot manufacture

A risk analyst who tells her colleagues "this tool actually makes the SR 11-7 documentation easier" carries more weight than any executive communication.

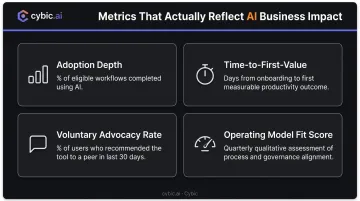

Measuring What Actually Matters

Login rates and training completions are not adoption. They are activity metrics that tell you nothing about whether AI is delivering value.

The meaningful metric is adoption depth: what percentage of eligible workflows are actually being completed using AI?

For banking teams, that means asking specific questions. What share of fraud alerts are reviewed using the AI prioritization queue? What proportion of credit memos are drafted with AI assistance? That number predicts business impact - login rates do not.

McKinsey's five-layer AI measurement framework covers adoption, operations, and financial results - a useful structure for consolidating AI reporting into a coherent value narrative rather than a dashboard of disconnected KPIs.

Three additional metrics worth tracking alongside adoption depth:

- Time-to-first-value: Days from onboarding to a user's first measurable productivity outcome. Shorter cycles accelerate word-of-mouth adoption across teams.

- Voluntary advocacy rate: Share of current users who have recommended the tool to a peer in the past 30 days - a leading indicator of organic scaling before formal rollout expands.

- Operating model fit score: A quarterly qualitative assessment of how well processes, decision rights, and accountability structures support the AI tool. Scores below threshold signal structural debt in processes and governance, not just a change management gap.

When executives see adoption depth, time-to-value, and net value realized in a single view, AI shifts from a technology update into a business conversation - one with clear ownership, clear outcomes, and a path to scaling.

Frequently Asked Questions

Frequently Asked Questions

Why do most AI initiatives in banking fail to scale beyond the pilot phase?

Pilots succeed in controlled conditions with clean data and cooperative teams - conditions that don't reflect enterprise banking operations. At scale, operating models aren't redesigned, ownership fragments across risk and business functions, and incentive structures continue rewarding old behaviors. These are organizational failures, not technical ones.

How do banks manage employee resistance to AI adoption?

Resistance in banking is often rational: staff face real accountability risk when AI touches regulated decisions. Effective change management reframes AI as augmentation rather than replacement, brings skeptics into co-design sessions, and addresses identity and fairness concerns head-on - not as a communications gap to be managed.

What change management frameworks work best for AI adoption in banking?

ADKAR (individual transition stages: Awareness, Desire, Knowledge, Ability, Reinforcement) and Kotter's 8-Step Model (organizational momentum) are the most commonly applied. Both require adaptation for banking - specifically ensuring governance and compliance are built into the change architecture from the start, not added as a final review gate.

How should banks engage compliance teams during AI transformation?

Compliance should be involved from day one as a co-designer, seated in the AI steering committee with veto power and a mandate to find solutions, not just flag risks. Banks that treat compliance as an end-gate create predictable bottlenecks; those that integrate it early build faster and more durable AI programs.

What metrics should banking leaders use to measure AI change management success?

Adoption depth (share of eligible workflows using AI), time-to-first-value per user, voluntary advocacy rate, and net value realized. Login rates and training completions are activity metrics. They don't correlate with business outcomes and shouldn't anchor executive reporting.

How long does a full AI change management program typically take in a bank?

A well-structured program runs 12–18 months: the first eight weeks on organizational assessment, months three through six on foundation building, and wave-based deployment thereafter. Change management should become a permanent function, not a project with a defined end date.