Introduction

Most financial institutions don't have a technology problem - they have a coordination problem. Core banking platforms, ERPs, CRMs, treasury systems, and compliance tools all run in parallel, each doing their job, none of them talking to the others.

Every financial process - an invoice approval, a KYC check, a credit decision - triggers a chain reaction across systems that were never built to coordinate.

API connectivity solved the data transfer problem. But connectivity without coordination leaves institutions with faster failures and harder-to-trace errors. The real challenge is governing what happens across those connections: who acts, in what sequence, under what rules, and with what audit record.

This guide covers what workflow orchestration actually means in a financial services context, why it's a distinct discipline from basic automation, where it delivers the most value, and what a well-built implementation looks like in practice.

Key Takeaways

- Workflow orchestration sequences, governs, and connects systems, people, and AI decisions across the full operation - not just isolated tasks

- Regulators audit the full decision chain in financial services - orchestration is what makes that chain auditable

- Annual financial crime compliance costs hit $61B in the US and Canada - KYC/AML is one of the highest-ROI targets for orchestration

- AI works best as a governed component inside an orchestrated workflow, not as a standalone decision layer

- Data sovereignty requirements disqualify cloud-only solutions for many institutions - infrastructure-agnostic deployment is a hard requirement

What Is Workflow Orchestration in Financial Services?

Workflow orchestration is the coordinated, rule-governed management of end-to-end financial processes that span multiple systems, teams, and decision points. Rather than automating a single task, it governs the entire sequence - from initiation through execution, exception handling, and audit - as one coherent, traceable flow.

The Control Plane Concept

Think of orchestration as a layer that sits above your existing tools - ERP, CRM, banking APIs, compliance platforms - coordinating them rather than replacing them. It provides the process logic those tools lack: context, sequencing, exception routing, and a complete record of every action.

Without this layer, each system handles its own slice. Bridging those gaps falls to people - and that's where errors, delays, and audit failures accumulate.

What Makes Financial Services Orchestration Different

General workflow tools can sequence tasks. Financial orchestration operates under a stricter set of constraints that most generic platforms weren't designed to meet:

- Multi-system dependencies - a single process may touch ERP, bank APIs, treasury platforms, and compliance tools in sequence

- Regulatory audit requirements - every decision, approval, and exception must be traceable end-to-end

- Strict data governance - role-based access, encrypted handling, and no leakage between process boundaries

- Mixed decision types - automated rules and human approvals must coexist within a single traceable flow

Five Structural Components of Financial Workflow Orchestration

Any orchestration system built for financial services needs all five:

- Unified data ingestion - consolidate inputs from all source systems before any process logic executes

- Execution logic - conditional branching, parallel processing, and rule-based routing built into the flow

- Governed access control - role-based restrictions on who can view, approve, or override at each step

- Structured exception handling - escalation paths triggered automatically when anomalies, compliance flags, or approval failures arise

- Full traceability - an unbroken audit record of every action, decision, and system state change

What most financial firms have today is fragmented automation - isolated steps covered by point solutions, with manual handoffs filling the gaps. That distinction matters when regulators ask for a complete process record.

Why Financial Services Needs Dedicated Workflow Orchestration

The Legacy Fragmentation Problem

Financial institutions typically run processes across core banking platforms, ERPs, CRMs, treasury management systems, and compliance tools. Each is a separate data silo with no unified process logic connecting them.

Data moves between systems through manual exports, email handoffs, or point-to-point integrations that nobody owns end-to-end.

The result: processes that appear automated but operationally still depend on individuals knowing which system to check next.

The ERP-Bank Visibility Gap

Banks and financial platforms see transactions. They generally don't see the purchase orders and sales orders sitting upstream in client ERPs - the data that represents future cash flows. That structural blind spot limits lending intelligence, risk signaling, and the ability to deliver proactive financial services. Connecting those upstream operational signals to real-time AR/AP and banking positions is one of the clearest orchestration opportunities in the sector.

The Regulatory Compliance Imperative

Financial services operates under frameworks that don't allow compliance to be an afterthought: SOX, DORA, AML/BSA, BCBS 239, and KYC requirements all impose specific process controls. Key mandates include:

- PCAOB AS 2201: Auditors must trace transactions through systems from origination to financial records

- DORA: Requires a documented ICT risk management framework

- 31 CFR 1020.210: Mandates AML programs with demonstrable internal controls

The SEC charged 11 Wall Street firms in 2023 with recordkeeping failures, resulting in $289 million in combined penalties. The Federal Reserve assessed Deutsche Bank $186 million for AML control weaknesses. These aren't edge cases - they reflect what happens when process governance isn't embedded in the architecture.

The False Automation Problem

According to Ardent Partners' 2024 AP benchmark, most finance operations are further from automation than they appear:

| Metric | Current Average | Best-in-Class |

|---|---|---|

| Invoices received manually | 49.7% | - |

| Straight-through processed | 32.4% | - |

| Exception rate per invoice | 20.7% | - |

| Cost per invoice | $9.87 | $2.81 |

The gap between average and best-in-class is a coordination problem, not a technology one. Approvals happen in messaging apps, exceptions get tracked in spreadsheets, and handoffs rely on institutional knowledge rather than system logic. Orchestration replaces that invisible coordination layer with defined, auditable process flows.

Key Use Cases: Where Workflow Orchestration Delivers in Finance

Accounts Payable and Receivable

An orchestrated AP/AR flow handles the full sequence as one governed process:

- Invoice receipt via email, portal, or EDI

- AI-driven data extraction and supplier validation

- Cost center matching and routing to appropriate approvers

- ERP posting upon approval

- Payment scheduling and bank confirmation

- Dashboard status updates and exception escalation if any step fails

No manual loops. No one chasing approvals in a chat thread. Every step logged.

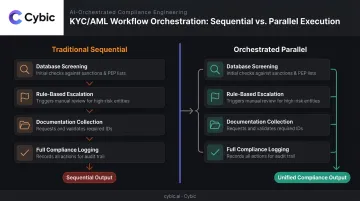

KYC, AML, and Customer Onboarding

Manual KYC is slow and expensive. Thomson Reuters reports business client onboarding historically took up to 48 days, with banks spending an average of $60 million annually on KYC compliance. The 2024 LexisNexis study puts total US and Canadian financial crime compliance costs at $61 billion, with 99% of institutions reporting cost increases and 70% actively prioritizing reduction.

Orchestration converts KYC from a sequential bottleneck into a parallel process. Key capabilities include:

- Simultaneous screening across multiple databases

- Rule-based escalation for high-risk flags

- Automated documentation collection

- Full compliance logging for every decision - with the audit trail built into the process in real time, not reconstructed afterward.

Credit Underwriting and Loan Origination

Manual underwriting involves the same data moving between people across too many systems. Orchestration coordinates document collection, credit scoring inputs, risk assessment, and multi-party approval routing as one governed flow - removing handoffs between underwriting, compliance review, and decisioning teams.

The practical impact: shorter cycle times and teams spending time on judgment rather than data entry. McKinsey's research on SME lending confirms that real-time transaction and sales data can sharpen credit models - but only if that data can be accessed and processed within a governed workflow.

Regulatory Reporting and Financial Close

End-of-period scrambles are a symptom of disconnected systems. Orchestrated reporting workflows handle scheduled data aggregation from multiple sources, apply validation rules automatically, flag exceptions for human review, and produce submission-ready outputs with a complete data lineage record.

BCBS 239 requires documented, validated risk-data aggregation with demonstrable accuracy and timeliness. That standard can't be met by a process that depends on someone manually pulling exports from three systems the night before a deadline.

Cash Flow Forecasting and Treasury Operations

The same data gaps that create reporting headaches show up in forecasting, too. Treasury teams working from bank statements alone are operating on lagging signals. Connecting upstream ERP data (purchase orders, sales orders) with real-time AR/AP pipelines and banking positions creates the conditions for proactive cash management rather than reactive transaction reconciliation.

PwC's 2025 Global Treasury Survey reports 74% of treasury respondents are expanding or actively using AI - but only 26% rate their AI capabilities as moderately or very mature. The constraint is the data infrastructure and process governance underneath the AI, not the AI itself.

Workflow Orchestration vs. Basic Automation: What's the Real Difference?

The distinction matters more in financial services than anywhere else.

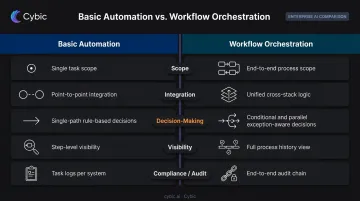

Scope and Integration Depth

| Dimension | Basic Automation | Workflow Orchestration |

|---|---|---|

| Scope | Single task or narrow step | End-to-end process across systems |

| Integration | Point-to-point between two systems | Unified logic across full technology stack |

| Decision-making | Rule-based, single path | Conditional, parallel, exception-aware |

| Visibility | Step-level status | Process-level view with full history |

| Compliance/Audit | Task logs per system | End-to-end audit chain across all steps |

Point-to-point automation creates connections. Orchestration creates a process: dependencies, conditional logic, parallel execution paths, and cross-system handoffs all managed from a single control layer.

Why the Distinction Matters for Compliance

Deloitte's 2022 Intelligent Automation survey found 74% of organizations implementing RPA - but the average intelligent automation maturity score was 5.04 out of 10. Most organizations have bots. Few have governed, end-to-end process coverage.

That gap is a compliance exposure. Isolated automations can complete individual steps correctly while leaving the overall process ungoverned. Regulators don't audit steps. They audit the decision chain. A firm that can prove each task ran correctly but can't demonstrate how an exception moved from detection to resolution has a governance problem, not a task-automation problem.

Only orchestration provides the end-to-end traceability that financial compliance requirements actually demand.

How AI Fits Into Financial Workflow Orchestration

AI as a Component, Not a Replacement

The correct model: AI handles document reading, data extraction, anomaly detection, classification, and preliminary risk assessment. The workflow provides governance, sequencing, escalation routing, and the audit record. Neither replaces the other.

The Bank of England/FCA 2024 survey found 75% of UK financial services firms already use AI, up from 58% in 2022. That adoption is outpacing governance maturity. That gap is where risk accumulates.

The Auditability Problem with AI Agents

When an AI agent triggers a payment, flags a transaction, or contributes to a credit decision, the audit chain must still be followable. What data did it act on? What logic did it apply? What was the result?

OCC/Federal Reserve/FDIC model risk guidance requires that model documentation be detailed enough for a knowledgeable third party to understand construction and limitations - and that model risk frameworks be periodically audited.

The orchestration layer is what makes that requirement achievable. It logs the originating signal, the AI's reasoning path, and the resulting action - creating the audit record that the AI component itself doesn't produce.

Governance by Design

For AI to operate safely in financial workflows, governance can't be a configuration option. Role-based access controls, encrypted data handling, and auditability of AI-driven actions need to be built into the architecture.

Cybic's Drava platform is structured around this principle. It combines AI reasoning and intelligent agents with governance controls embedded at the architectural level:

- Role-based access controls (RBAC) governing who can trigger, view, or modify workflows

- Encrypted data protection in transit and at rest

- Full traceability of every AI-driven action, tied to the originating signal and outcome

This architecture is built for regulated financial environments from day one - not retrofitted after deployment.

What to Look for in a Financial Workflow Orchestration Solution

Three criteria separate solutions that work in financial services from ones that look good in demos:

1. Governance embedded at the architectural level Ask vendors specifically how compliance is embedded in system design - not what compliance features appear in the UI. Auditability, access controls, and regulatory alignment need to be foundational, not optional. Cybic's approach builds security controls, RBAC, audit trails, and data governance directly into every engagement from day one.

2. Infrastructure-agnostic deployment Data sovereignty and data residency requirements are real constraints for financial institutions. A solution that only works in a single cloud environment isn't viable for firms with on-premises processing requirements or cross-border operations. Cybic's Drava platform supports cloud, hybrid, and on-premises deployment without locking institutions into a single infrastructure model.

3. Engineering-led, operationally grounded implementation The gap between a working demo and a production system is where most orchestration projects stall. Look for partners who design around your existing infrastructure, legacy constraints, and compliance requirements from the first conversation - not teams who hand off integration work after delivering a prototype. Cybic's engineers architect, build, and integrate directly into the environments financial teams actually operate in - not after a handoff, but from the first conversation.

Frequently Asked Questions

What is an orchestration workflow?

An orchestration workflow is the coordinated management of a multi-step process across systems and teams, where a central logic layer controls sequencing, decisions, exceptions, and handoffs. It ensures the entire process runs consistently and with full traceability - not whether individual steps complete, but how they connect into a governed whole.

What are the four types of workflows?

The four common types are sequential (steps run in fixed order), parallel (steps run simultaneously), conditional (branching based on rules or outcomes), and loop-based (steps that repeat until a condition is met). Financial orchestration combines all four within a single process.

How is RPA used in finance?

RPA handles repetitive, rule-based tasks such as data entry, invoice extraction, and report generation, but operates at the task level. Workflow orchestration sits above RPA - sequencing, governing, and connecting bots with other systems and human decisions into a complete, auditable process.

Which integration service is used to create workflows and orchestrate?

Financial workflow orchestration platforms connect to existing systems via APIs, middleware, or native connectors. The orchestration layer sits above individual integration services, managing end-to-end process logic rather than point-to-point data transfer.

What is the difference between workflow automation and workflow orchestration?

Workflow automation handles individual steps or tasks in isolation. Workflow orchestration coordinates the entire end-to-end process, managing how tasks, systems, people, and decisions interact across the full sequence with unified visibility, governance, and exception handling.

How does workflow orchestration support compliance in financial services?

Orchestration creates a single, auditable record of every step, decision, approval, and system action within a process. When regulators ask what happened, when, and why, that answer already exists - no manual reconstruction from disconnected system logs required.