Introduction

Financial institutions process staggering document volumes every day. The CFPB's 2023 HMDA data covered 10 million home-loan applications and 11.5 million total records. FinCEN reported 4.7 million Suspicious Activity Reports and 20.5 million Currency Transaction Reports in FY2024 alone. Behind each of those filings sits a stack of documents that someone, somewhere, has to touch.

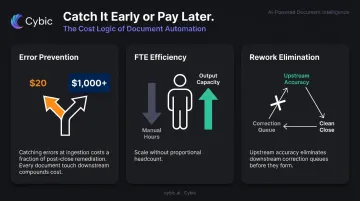

Manual handling also carries a measurable accuracy cost. MBA-hosted mortgage research found that human classification and extraction accuracy averages only 80%, with early-stage error rates of 10–15%. A $20 mistake caught during origination can exceed $1,000 in remediation costs if it surfaces at closing.

Automation addresses each of these pressure points. This guide covers what financial document automation is, where it delivers the most value, what benefits institutions can realistically expect, and what to evaluate before selecting a solution.

Key Takeaways

- Document automation uses AI, OCR, and workflow orchestration to handle document-heavy financial processes with minimal manual intervention.

- Key use cases: loan origination, KYC/AML compliance, mortgage processing, claims management, and account onboarding.

- Results include faster cycle times, lower error rates, reduced operational costs, and stronger audit readiness.

- Legacy integration, data security, and change management are the primary challenges - all with well-defined mitigation approaches.

- When evaluating solutions, prioritize extraction accuracy, integration depth, compliance certifications, and governance architecture.

What Is Document Automation in Financial Services?

Document automation in financial services covers the full lifecycle of financial documents - creation, ingestion, extraction, validation, routing, and storage - with little to no manual intervention. It runs on a stack of AI, machine learning, NLP, OCR, and workflow orchestration technologies working in concert.

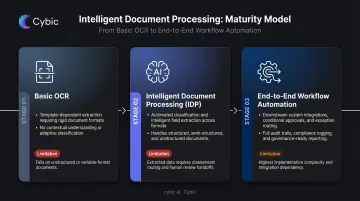

Three Tiers of Maturity

Not all document automation is equal. There's a meaningful difference between the three tiers:

| Tier | What It Does | Limitation |

|---|---|---|

| Basic OCR | Converts scanned images to machine-readable text | Requires rigid templates; no contextual understanding |

| Intelligent Document Processing (IDP) | Classifies document types, extracts fields, validates data regardless of format | Extraction errors can still enter downstream systems |

| End-to-end workflow automation | Connects IDP to downstream systems, approvals, routing, and audit trails | Requires strong governance and vendor controls |

Institutions that stop at OCR capture only a fraction of the potential value. The real gains come from IDP connected to workflow execution - where extracted data flows directly into loan origination systems, KYC platforms, or claims management tools without manual rekeying.

Why Financial Services Is High Stakes

The regulatory and operational environment makes this domain particularly unforgiving:

- KYC, AML, GDPR, SOC 2, and GLBA Safeguards each impose distinct documentation and auditability requirements

- Errors on high-volume PII documents aren't just operational problems - they create direct compliance exposure

- Regulators expect complete, traceable records of every document action, not just outcomes

- Processing delays on loan applications or claims translate into measurable revenue loss and client attrition

Key Use Cases of Document Automation in Financial Services

Loan Origination and Underwriting

Borrowers submit pay stubs, bank statements, tax returns, identity proofs, and credit reports. Underwriters manually reviewing these stacks create backlogs, introduce inconsistency, and delay revenue recognition.

Automation handles the full intake sequence:

- Ingests and classifies each document type on arrival

- Extracts key data fields and validates against predefined credit rules

- Flags exceptions for underwriter review

- Routes clean data directly to the loan origination system

The same MBA research shows AI-powered OCR hits ~95% accuracy out of the box, reaching 99%+ after training on proprietary data, compared to 80% for manual review.

For syndicated loans, McKinsey found that automation leaders achieve 80–90% straight-through processing rates, with modernization lifting productivity by 20–50%.

KYC and AML Compliance

Manual KYC and AML processes create compliance gaps that are hard to close at scale. Collecting, verifying, and continuously monitoring identity documents, beneficial ownership records, and transaction files generates enormous review volume with limited audit transparency.

The cost pressure is severe. LexisNexis Risk Solutions estimates U.S. and Canada financial-crime compliance costs reached $61 billion in 2024, with 99% of institutions reporting rising costs. McKinsey's KYC research shows low-risk periodic reviews average 100 minutes - but best-quartile performers using straight-through processing on 50–65% of files complete the same reviews in 30 minutes.

Automated document workflows address this directly:

- Capture and classify identity documents at intake

- Run validation checks against sanctions and watchlists

- Generate timestamped audit trails for every document action

- Flag anomalies for escalation without manual triage

The result is compressed review time and a defensible, auditable compliance record.

Mortgage Processing and Insurance Claims

Mortgage processing carries one of the heaviest document burdens in financial services: appraisal reports, title documents, employment verification, income statements, and disclosure forms all require review before a loan can close. The average time to close stood at 49 days as of mid-2021 (ICE Mortgage Technology). IDP platforms compress application review from days to hours, and Fannie Mae data shows automated income, employment, and asset validation can reduce repurchase risk by 64%.

Insurance claims introduce a different challenge: ingesting loss notices, medical records, repair estimates, and policy documents from multiple sources in varying formats. One IBM case study shows a claims administrator scaling from 15 claims per day to 288 claims per day - a 20x productivity gain with 4x faster cycle times - by automating document extraction from complex, paper-heavy files.

Account Opening and Compliance Reporting

Account onboarding requires ID verification, address confirmation, signature capture, and risk profiling. Automation consolidates document intake via digital portals, validates data in real time, and routes completed files for approval or e-signature, enabling straight-through processing for qualified applicants.

The cost of slow onboarding is measurable: Fenergo's 2025 survey found 70% of institutions reported losing clients due to slow onboarding processes, with UK corporate bank onboarding averaging over six weeks.

Compliance reporting teams see a different kind of benefit. Rather than manually assembling audit packages, automation handles:

- Populating compliance report templates from structured document data

- Maintaining version-controlled records across the document lifecycle

- Generating audit-ready trails that log who accessed, modified, or approved each document and when

Benefits of Document Automation for Financial Institutions

Speed and Throughput

Automation compresses multi-day manual workflows into hours by eliminating manual data entry, queuing delays, and handoff bottlenecks. National Bank of Greece offers a concrete benchmark: after implementing Azure AI Document Intelligence, NBG processes 700,000+ pages per month across 50+ document types at 0.5 seconds per page - deployed in under four months.

Cost Reduction

Automating document-heavy processes reduces FTE hours spent on low-value extraction and rekeying, cuts rework from errors, and scales volume capacity without proportional headcount increases. The strongest cost argument, though, is loss avoidance. The $20-to-$1,000+ error escalation pattern in mortgage processing shows how catching mistakes at ingestion prevents far more expensive downstream remediation.

Accuracy and Error Reduction

AI-powered extraction pulls data directly from source documents into downstream systems, eliminating duplicate records, transposed digits, and copy-paste errors. At scale, those gains compound across the operation:

- Fewer rework cycles and correction queues

- Fewer compliance violations from data entry mistakes

- Fewer customer-facing errors reaching downstream systems

Regulatory Compliance and Auditability

Automation enforces consistent process execution across every document, applies business rules uniformly, and generates immutable audit trails. For institutions subject to OCC third-party risk guidance, CFPB data protection requirements, and SOC 2, this consistency is the difference between a clean audit and a remediation effort.

That compliance posture only holds if the underlying system is built for it. Cybic embeds controls like RBAC, end-to-end encryption, audit logging, and a no-client-data-training policy directly into the architecture - not as add-ons applied after deployment. Regulators increasingly scrutinize how a system was built, not just what it produces, and that architectural rigor is where audits are won or lost.

Common Challenges and How to Overcome Them

Legacy System Integration

Most financial institutions run document workflows on core banking platforms with limited API capability. Modern automation tools need to connect to these systems without requiring full platform replacement.

Mitigation: Use a middleware or API layer to bridge legacy infrastructure with new automation tooling. Cybic's legacy modernization and ecosystem integration services follow this pattern: custom API development connects existing core banking systems to intelligent document workflows while keeping live operations intact. Prioritize vendors with pre-built connectors for common financial infrastructure and flexible API access for custom integrations.

Data Security and Regulatory Risk

Financial documents contain sensitive PII subject to SOC 2, GDPR, CCPA, and GLBA Safeguards requirements. The FTC has specifically warned that AI vendors must honor privacy commitments - and that models built with unlawfully obtained data can be subject to deletion orders.

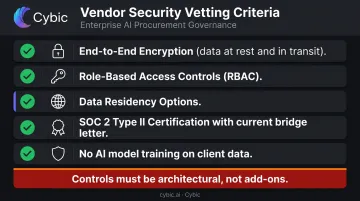

Key vendor vetting criteria:

- End-to-end encryption (data at rest and in transit)

- Role-based access controls (RBAC)

- Data residency options

- SOC 2 Type II certification with current bridge letter

- Explicit policy confirming client data is not used to train AI models

Security and governance controls need to be built into the system architecture at the design stage, not bolted on after deployment as an afterthought.

Change Management and User Adoption

Automation initiatives often stall not because the technology fails, but because staff resistance and poorly designed rollouts prevent adoption.

- Pilot one high-friction workflow first to build a measurable proof of value

- Involve end users - underwriters, compliance officers, ops teams - in workflow design

- Select tools with interfaces that require minimal technical training

- Secure broader organizational commitment only after early wins are documented

What to Look for in a Financial Document Automation Solution

Extraction Accuracy Across Unstructured Formats

Published benchmarks show accuracy ranging from ~90% in production bank deployments to 99%+ after mortgage-specific model training. The key is validating accuracy on your institution's own documents, not just vendor-supplied test sets.

Avoid platforms that require extensive manual template configuration for each new document type - this creates scaling bottlenecks that defeat the operational efficiency argument.

Integration Depth

Automation tools that create new data silos undermine the value they're supposed to deliver. Look for:

- Pre-built connectors to core banking systems, loan origination platforms, CRMs, and ERPs

- Flexible API access for custom integrations

- Real-time data sync that eliminates manual data transfer

Governance and Security Architecture

For financial institutions, these controls are mandatory:

- SOC 2 Type II certification (current, not expired)

- RBAC with documented access policies

- End-to-end encryption for data at rest and in transit

- Full audit logging of every system action

- Explicit policy that vendor does not train AI models on proprietary client data

Cybic builds these controls directly into its automation architecture - governance, access management, and auditability are structural properties of the system, present from the first deployment rather than added after the fact.

Scalability and Deployment Flexibility

Financial institutions often need private cloud or on-premises deployment for data sovereignty. Large institutions cannot accept SaaS-only platforms that conflict with their data governance policies.

The right solution supports your required deployment model and scales with document volume. Confirm the platform offers:

- Cloud, hybrid, and on-premises deployment options

- Performance that holds under high document throughput

- No data residency compromises for regulated environments

Human-in-the-Loop Exception Handling

Full automation is rarely appropriate for high-stakes financial decisions. The best platforms include configurable exception routing: edge cases, low-confidence extractions, and rule violations surface to human reviewers, while standard cases proceed automatically.

This balance is what makes automation viable in regulated environments.

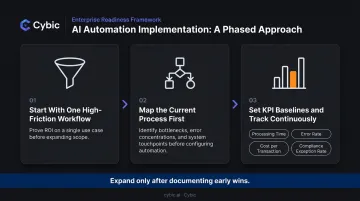

Implementation Best Practices

Start with one high-friction workflow. Pick a single process - bank statement ingestion for loan underwriting or invoice processing for accounts payable - where manual effort is highest and document formats are relatively consistent. Prove ROI before expanding scope.

Map the current process before configuring anything. Document who touches each document, which systems are involved, where queues build up, and where errors concentrate. Automation layered over a flawed manual process doesn't fix the flaws - it locks them in.

Set KPI baselines before go-live, then track continuously. Establish benchmarks across four key metrics before deployment:

- Processing time per document

- Error rate

- Cost per transaction

- Compliance exception rate

Regular monitoring confirms the system is performing against business goals - and gives you the data to justify expansion.

Frequently Asked Questions

How do you automate financial processes?

Identify high-volume, document-heavy workflows - loan processing, compliance reporting, claims intake - then select an AI-powered document automation platform that integrates with your existing systems. Deploy in phases: start with one defined use case, measure results, and expand from there.

What documents can be automated in financial services?

Bank statements, loan applications, tax returns, pay stubs, identity documents (KYC), insurance claims forms, invoices, contracts, mortgage documents, compliance reports, and audit files. Modern IDP platforms handle both structured and unstructured formats, including handwritten forms and multi-page statements.

What is the difference between document automation and RPA?

RPA mimics rule-based human actions on existing interfaces (clicking, copying, pasting) without understanding document content. Document automation uses AI and IDP to actually read, interpret, classify, and extract data from documents. That distinction makes it far better suited for the variable, unstructured documents common in financial services.

How does document automation support regulatory compliance?

Automation enforces consistent process execution across every document, generates immutable audit trails, and applies compliance rules uniformly. Record retrieval becomes straightforward during regulatory audits, reducing both the cost and operational burden of compliance management.

Is document automation secure enough for sensitive financial data?

Enterprise-grade platforms include end-to-end encryption, RBAC, SOC 2 certification, and data residency options. Before selecting a vendor, confirm they do not train AI models on client data - this is a common and underappreciated risk that financial institutions frequently overlook during procurement.

How long does implementation take?

A focused deployment on a single workflow can go live in weeks. Enterprise-wide rollouts involving legacy system integration typically take several months. Starting with one high-impact use case and expanding in phases is the most reliable way to build momentum while managing integration risk.