Introduction

According to the Federal Reserve's 2024 Payments Study, US financial institutions processed 89.1 billion non-prepaid debit card payments and 58.5 billion credit card transactions in 2022 alone - before counting ACH transfers, wire payments, and internal reconciliations.

Managing that volume while satisfying AML, KYC, SOX, and GDPR requirements, and cutting operational costs, is difficult. Basic RPA helped for a while. But rule-based bots break when formats change, can't handle unstructured data, and require manual updates to catch new fraud patterns.

Intelligent process automation (IPA) addresses these gaps by combining RPA with AI, machine learning, and natural language processing - creating systems capable of judgment and exception handling, not just repetitive data entry.

This guide covers what IPA is, where it delivers the most value in finance, how to implement it, and what challenges to prepare for.

Key Takeaways

- IPA combines RPA with AI and ML to handle complex, judgment-intensive workflows - not just rule-based tasks

- Highest-impact use cases: compliance reporting, fraud detection, invoice processing, financial forecasting, and KYC onboarding

- Top-performing AP teams achieve invoice processing costs 78% lower than peers through automation maturity

- Start with 1-2 high-value pilots - data governance and compliance controls should be built in from the start, not added later

- In regulated financial environments, governance, auditability, and security are prerequisites, not afterthoughts

What Is Intelligent Process Automation in Financial Services?

Gartner defines IPA as the use of AI and machine learning to automate and optimize business processes. In financial services, that means automating entire workflows end-to-end: including processes that require pattern recognition, contextual judgment, and dynamic exception handling.

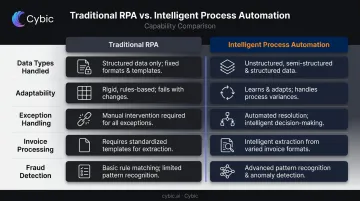

Intelligent Automation vs. Traditional RPA

The distinction matters practically, not just conceptually:

| Capability | Traditional RPA | Intelligent Process Automation |

|---|---|---|

| Data types handled | Structured, fixed-format only | Structured and unstructured |

| Adaptability | Breaks on format changes | Learns and adapts |

| Exception handling | Escalates everything | Resolves most cases autonomously |

| Example | Extracts invoice data from one fixed template | Extracts and validates data across hundreds of inconsistent vendor formats |

| Fraud detection | Flags known rule violations | Identifies novel patterns through ML |

That table captures the core gap. As PwC puts it, RPA handles repetitive tasks with minimal input, while intelligent automation orchestrates a collection of tools to solve problems ranging from rules-based work through to complex data analysis and autonomous decision-making.

The Technology Stack Behind IPA

A full IPA architecture connects several layers:

- RPA - executes defined workflow steps and system interactions

- AI/ML - handles pattern recognition, anomaly detection, and predictive logic

- NLP - processes unstructured documents, communications, and contracts

- Process orchestration - connects systems, manages handoffs, and triggers actions

- Analytics - monitors performance and surfaces exceptions in real time

The challenge with multi-vendor approaches is integration debt: separate governance frameworks, visibility gaps between tools, and compliance controls that sit outside the automation layer rather than inside it.

Cybic's Drava platform is built specifically for this problem. It connects enterprise data, machine learning, AI reasoning, and intelligent agents in a single governed architecture - with security controls, role-based access, and auditability embedded at the system level rather than added as an afterthought.

Top Use Cases of IPA in Financial Services

Financial services is one of the most productive environments for IPA: high transaction volume, structured data, strict compliance requirements, and repetitive back-office workflows all create natural automation targets. Financial services is one of the most productive environments for IPA: high transaction volumes, structured data, strict compliance requirements, and repetitive back-office workflows all create natural automation targets. The five use cases below show where that impact is most measurable.

Regulatory Compliance and Automated Reporting

Financial crime compliance in the US and Canada costs $61 billion annually, according to LexisNexis Risk Solutions. A significant portion of that cost is manual - analysts reviewing transactions, assembling reports, and chasing documentation.

IPA changes the economics by:

- Continuously monitoring transactions against AML, KYC, Dodd-Frank, and GDPR rules

- Auto-generating compliance reports with timestamped, traceable records

- Flagging potential violations before they become formal findings

- Producing audit-ready documentation without manual assembly sprints

The auditability advantage is particularly significant. Regulators don't just want accurate reports - they want to see the process. Automated systems produce that evidence by default.

Fraud Detection and Anomaly Monitoring

Money laundering alone accounts for an estimated 2–5% of global GDP, roughly $800 billion to $2 trillion annually, according to BIS research on Project Aurora. The BIS project tested AI and ML-based collaborative analytics specifically for AML detection, finding that these approaches showed greater effectiveness at identifying suspicious networks than rule-based systems operating in isolation.

The practical advantage: ML models learn new fraud signatures from transaction history. Rule-based systems require manual updates every time a new pattern emerges. In financial services, where fraud tactics evolve continuously, that gap in adaptability is a direct operational risk.

Invoice Processing and Accounts Payable/Receivable

The average enterprise spends $9.87 to process a single invoice - but best-in-class AP teams achieve costs 78% lower than their peers, according to Ardent Partners' 2024 research.

IPA closes that gap through:

- OCR and NLP to extract invoice data regardless of vendor format

- Automated PO matching and three-way reconciliation

- Exception routing to human review only when needed

- Faster close cycles and reduced late payment exposure

Cybic's Intelligent Document Processing capability handles this across inconsistent vendor formats, which is a consistent pain point in AP workflows where dozens of templates are in active use.

Predictive Forecasting and Financial Planning

Finance AI adoption doubled in a single year: 58% of finance functions were using AI in 2024, up from 37% the prior year, according to Gartner. The performance difference shows up in forecast quality - FP&A teams using AI or ML rate their forecasts as great or good at a 65% rate, compared to just 42% among teams not using these tools.

Unlike static spreadsheet models, IPA-connected forecasting updates automatically as actuals arrive and surfaces variance alerts in real time. Teams act on current data instead of correcting course after month-end close.

Customer Onboarding and KYC Automation

Fenergo's 2024 banking research found that 48% of banks experienced client abandonment during onboarding - a direct revenue consequence of slow, manual KYC processes.

IPA addresses this by automating:

- Identity verification and document collection

- Credit screening and risk scoring

- AML checks and enhanced due diligence workflows

- Continuous monitoring post-onboarding

Cycle times that previously took days compress to hours. The compliance posture doesn't weaken - the process simply stops depending on manual coordination between teams.

How to Implement IPA in Financial Services: A Practical Approach

Step 1: Process Mapping and Prioritization

Before selecting any technology, audit existing workflows. Identify where volume is highest, error rates are greatest, and manual effort is most costly. Then choose 1-2 pilots - AP automation and compliance reporting are reliable starting points - rather than attempting a broad simultaneous rollout.

Starting narrow isn't a limitation. It's how you prove ROI quickly and build internal confidence before scaling.

Step 2: Data Readiness and Governance Foundation

IPA systems are only as reliable as the data feeding them. Before automating a workflow, establish:

- Data quality standards and validation rules

- Access controls and role-based permissions

- Data lineage tracking from source to output

- Policies governing how data flows through AI models

In regulated environments, governance embedded at the architecture level is non-negotiable. Cybic builds security controls, RBAC, auditability, and data governance directly into system architecture. A strict policy ensures no proprietary enterprise data is used to train external models - a critical requirement for financial services clients.

Step 3: Integration with Existing Systems

Financial institutions rarely need to replace existing ERP, CRM, or core banking systems. The right IPA platform connects to that infrastructure through APIs and integration layers - not rip-and-replace.

Cybic's ecosystem integration services connect AI platforms, data pipelines, and enterprise applications across AWS, Azure, and Google Cloud - as well as hybrid and on-premises environments. This avoids vendor lock-in and fits the layered IT infrastructure common in banking and financial services.

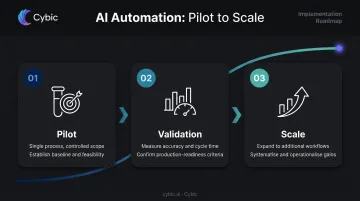

Step 4: Phased Deployment and Change Management

A staged rollout reduces risk and surfaces edge cases before they affect production:

- Pilot phase - single process, limited scope, controlled environment

- Validation phase - measure accuracy, cycle time, exception rates against baseline

- Scale phase - expand to additional workflows and business units based on validated results

Technical deployment is only half the work. Finance teams whose roles shift from data preparation to decision-making need structured communication about what's changing and why - without that, adoption stalls regardless of how well the system performs.

Step 5: Continuous Monitoring and Optimization

After go-live, ongoing monitoring is essential. Track:

- Processing time and throughput

- Error and exception rates

- Compliance incidents

- Model drift in AI components

Build a feedback loop where edge cases that reach human review inform ongoing model improvements. Cybic embeds MLOps pipelines - including automated model retraining, model versioning, and performance monitoring - into deployments to keep AI components performing accurately.

Common Implementation Challenges and How to Navigate Them

Legacy System Integration Complexity

Older core banking and ERP systems often lack modern APIs. Deloitte notes that legacy systems are difficult to maintain and that banks need modernization strategies to support new capabilities.

Start with middleware connectors or RPA as a bridge layer while building a longer-term modernization roadmap. Engage implementation partners with demonstrated financial services infrastructure experience - general-purpose automation vendors routinely underestimate the complexity specific to banking environments.

Data Privacy, Security, and Regulatory Compliance

IPA systems need access to sensitive financial data to function. That creates exposure if security controls are insufficient. Relevant requirements include:

- GLBA Safeguards Rule - written information security program with access controls, encryption, and monitoring

- SOX/ICFR - automated controls affecting financial reporting require design and operating-effectiveness evidence

- PCI DSS - controls covering cardholder data environments, access, logging, and incident response

- GDPR Article 32 - encryption, confidentiality, availability, and regular testing

Addressing these requirements calls for controls at every layer:

- End-to-end encryption for data in transit and at rest

- Strict role-based access controls (RBAC) limiting system exposure

- Full auditability of AI-driven actions for regulatory traceability

- A documented policy that proprietary data is never used to train external models

Employee Resistance and Skill Gaps

Automation projects fail for organizational reasons as often as technical ones. Finance teams may resist IPA if it's framed as a replacement rather than a capability upgrade.

Involve finance teams in process design from the start, communicate clearly about how roles evolve, and invest in targeted upskilling. People who spend less time on data assembly and more time on analysis and advisory work tend to become advocates for the systems that made that shift possible.

Each of these challenges - integration complexity, data security, and organizational change - is manageable with the right architecture and implementation approach built in from day one.

Frequently Asked Questions

What is intelligent process automation in finance?

IPA combines RPA, AI, machine learning, and NLP to automate end-to-end financial workflows - including complex, judgment-intensive tasks like fraud detection and compliance reporting. It enables financial institutions to improve accuracy, reduce costs, and maintain compliance at scale.

What is the difference between RPA and intelligent process automation?

RPA executes rule-based tasks using fixed scripts and breaks when inputs change. IPA adds AI and ML to handle variability, unstructured data, and decision-making - enabling exception handling and continuous model improvement that static RPA scripts cannot support.

What financial processes are best suited for intelligent automation?

The highest-value starting points are compliance reporting, fraud detection, invoice and AP/AR processing, financial forecasting, and customer onboarding - all high-volume, data-intensive processes subject to strict accuracy and audit requirements.

What are the biggest challenges in implementing IPA in financial services?

The three most common obstacles are legacy system integration complexity, data security and regulatory compliance requirements, and organizational change management. Each requires a structured implementation plan that addresses infrastructure constraints, compliance controls, and stakeholder adoption from the start.

How does AI governance factor into financial services automation?

Governance ensures automated decisions are auditable, explainable, and compliant with regulatory requirements. In practice, this means:

- Role-based access controls limiting system exposure

- Data lineage tracking for full audit trails

- Encrypted data handling in transit and at rest

- Traceable logic linking every AI-driven output to its inputs

How long does it take to see ROI from an IPA implementation?

Most organizations see measurable ROI within the first year of a well-scoped pilot - especially in AP automation or compliance reporting. Broader enterprise-wide value typically accumulates over 18–36 months as automation scales across additional workflows.