Introduction: Why Financial Services Can't Afford to Wait

Three forces are colliding in financial services right now: customers expect personalized, on-demand digital experiences; fintech competitors built natively on modern infrastructure are eating into traditional market share; and regulators keep adding compliance requirements with no sign of slowing. Institutions that treat digital transformation as a future-state project are already behind.

The pressure is measurable. According to Gartner, only 48% of digital initiatives meet or exceed their business outcome targets - meaning most transformation efforts fall short, typically due to poor sequencing, governance gaps, or adoption failures. The difference between the 48% that succeed and the majority that don't usually comes down to how the work is structured, not how much is spent.

This guide covers what digital transformation actually means in financial services: the technologies driving it, how to build a phased roadmap, how to govern it under regulatory constraints, and how to measure whether it's working.

Key Takeaways

- Digital transformation in financial services means rebuilding how institutions create value, not just adding apps and portals

- AI, cloud, intelligent automation, and unified data platforms are the four foundational technology layers

- Governance must be embedded at the architecture level, not added after deployment

- Success requires quantifiable KPIs across customer experience, operational efficiency, and revenue impact

- Sprint-based delivery manages risk better and produces results faster than multi-year waterfall programs

What Is Digital Transformation in Financial Services?

Digital transformation in financial services is the comprehensive reimagining of business processes, customer experiences, and operating models through technology. Digitizing a paper form or moving a PDF to an online portal isn't transformation. Transformation means fundamentally rethinking how the institution creates value - and rebuilding the infrastructure to support it.

The Four Core Pillars

| Pillar | What It Means |

|---|---|

| Customer Experience | Personalized, omnichannel engagement across every touchpoint |

| Operational Excellence | Automated workflows that eliminate manual, high-volume processes |

| Data-Driven Decisions | Real-time analytics and predictive insight replacing gut-feel judgment |

| Business Model Innovation | New revenue streams and service models enabled by technology |

Each pillar reinforces the others. An institution that automates operations but ignores customer experience will cut costs without growing revenue. One that improves customer experience without fixing data infrastructure will overpromise and underdeliver.

What Makes Financial Services DX Uniquely Difficult

Financial institutions operate under a regulatory framework that most other industries don't face. Key regulations impose overlapping requirements that directly shape technology decisions:

- SEC Rule 17a-4 and FINRA 3110 - data retention and supervisory controls

- GLBA and SOX - access controls, financial reporting integrity, and audit trails

- GDPR - breach notification, data subject rights, and cross-border data handling

Technology selection in this environment is a compliance decision, not just a capabilities one.

Institutions that ignore this upfront pay for it later. Retrofitting compliance controls after deployment consistently costs more than embedding them at the architectural level. Every early-phase decision either builds compliance leverage or accumulates compliance debt.

Key Technologies Driving Digital Transformation in Financial Services

Artificial Intelligence and Machine Learning

AI and ML now sit at the center of financial services transformation. A 2024 Gartner survey found that 58% of finance functions are already using AI, with adoption accelerating across fraud detection, credit risk modeling, document processing, and personalized product recommendations.

The most immediate use cases include:

- Fraud detection - real-time transaction anomaly scoring at scale

- Credit risk modeling - predictive models trained on behavioral and financial data

- Document automation - intelligent extraction from loan applications, KYC documents, and contracts

- Customer service - AI agents handling routine inquiries and routing complex cases to advisors

For regulated institutions, the key requirement goes beyond AI capability: it's governed AI capability. Models making credit decisions or flagging suspicious transactions must be auditable, explainable, and monitored for bias.

Cloud Computing and API Architecture

Cloud infrastructure gives financial institutions the agility to scale operations without the capital burden of on-premise hardware. Public, hybrid, and private cloud models each serve different risk tolerances and regulatory requirements , and no single model fits every institution.

An API-first architecture is what makes cloud infrastructure operationally effective. APIs enable:

- Open banking integrations with fintech partners

- Real-time data sharing across systems and third parties

- Modular updates that don't require full platform replacements

Institutions that build with APIs at the core can swap components, add partners, and adapt to regulatory changes without rebuilding from scratch.

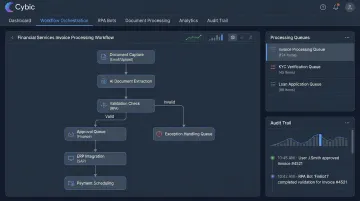

Intelligent Automation and Workflow Orchestration

Robotic process automation (RPA) and intelligent automation systems eliminate high-volume manual work that consumes thousands of staff-hours annually:

- Loan processing and KYC verification

- Compliance report generation and regulatory filings

- Client onboarding packet assembly

Cybic's intelligent automation practice covers RPA, Intelligent Document Processing (IDP), and agentic AI systems capable of goal-based workflow orchestration - including automated loan approval routing and intelligent claim processing. For financial institutions, the critical differentiator is governance: automation must maintain audit trails and respect access controls, not operate as a black box.

Data Analytics and Predictive Intelligence

Most financial institutions sit on enormous data reserves locked in silos : separate CRM systems, core banking platforms, custodial systems, and risk databases that don't talk to each other. Unifying these into a single source of truth is the prerequisite for any meaningful analytics capability.

Cybic's data engineering practice builds real-time ETL/ELT pipelines across AWS, Azure, Google Cloud, Snowflake, and Databricks, connecting siloed systems into unified platforms that support behavioral segmentation, predictive modeling, and real-time risk monitoring.

The technical architecture matters less than the outcome: financial advisors and risk teams should act on complete, current data rather than yesterday's export.

Blockchain and Emerging Technologies

Blockchain's practical foothold in financial services is in cross-border payments, trade finance, and digital asset custody : areas where tamper-resistant transaction records and smart contracts reduce reconciliation costs and counterparty risk. The BIS's Project Agorá is exploring tokenization of wholesale cross-border transactions at scale, signaling where institutional infrastructure is heading.

Biometric authentication and IoT-enabled security layers are also expanding how institutions verify identity and monitor account access , particularly relevant as mobile and API-based interactions replace branch visits.

How to Build a Digital Transformation Roadmap for Financial Services

Phase 1 - Assess and Define

Before selecting any technology, establish what you're trying to achieve. A credible assessment covers:

- Inventory of existing systems and integration dependencies

- Process inefficiency mapping (where are manual steps, error rates, and bottlenecks?)

- Customer pain points surfaced through data and direct research

- Target outcomes with specific metrics - reduce onboarding time by X%, increase digital channel adoption to Y%, improve advisor capacity by Z clients

Cybic's Digital Transformation Strategy practice structures this phase around AI and digital opportunity discovery, transformation roadmaps, and ROI advisory - because the assessment determines whether the roadmap reflects operational reality or just budget aspirations.

Phase 2 - Prioritize and Plan

Not all transformation initiatives carry equal risk or equal return. Sequence matters.

Start with high-volume, low-risk processes that have clear ROI:

- Document processing and extraction

- Client onboarding workflows

- FAQ and tier-1 support automation

Tackle complex system re-engineering - core banking replacements, full data warehouse migrations - after the team has built delivery capability and stakeholder confidence.

Build vs. buy vs. partner framework:

- Build proprietary capabilities that differentiate your institution: risk models, custom client analytics

- Buy commodity functions where off-the-shelf solutions are sufficient: email infrastructure, standard CRM modules

- Partner for specialized AI and compliance expertise where building internal capability would take too long

Phase 3 - Deploy AI and Automation with Governance at the Core

Governance frameworks belong in the deployment plan from day one. That means AI systems are architected to include:

- Role-based access controls (RBAC) managing permissions across operations teams

- Complete audit trails of AI-driven decisions for regulatory review

- End-to-end data encryption in transit and at rest

- Strict data governance - including a guarantee that proprietary enterprise data is never used to train AI models

This last point carries particular weight under GLBA and SEC data protection rules. When client financial data enters an AI system, where it goes and how it's used is a compliance question - one that needs an answer before deployment, not after.

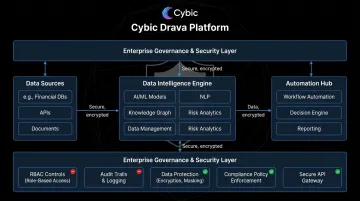

Cybic's Drava platform (an enterprise Data Intelligence to Automation platform connecting enterprise data, ML, AI reasoning, and intelligent agents) embeds these controls directly into its architecture. RBAC, audit trails, encrypted data protection, and strict data governance are foundational elements. For financial institutions, this is the baseline any AI deployment partner should meet.

Phase 4 - Modernize Customer Engagement

An omnichannel financial experience means seamless transitions between mobile apps, web portals, advisor calls, and branch interactions - without the customer having to re-explain their situation at each touchpoint.

The goal is not to replace advisors. It's to give them better tools. When an advisor walks into a client meeting with a complete behavioral profile, recent transaction context, and AI-surfaced product recommendations, the conversation is meaningfully different: higher value, better informed, more efficient.

Generative AI copilots and LLM-powered document intelligence systems (built on governed pipelines like Drava) support exactly this kind of advisor augmentation without exposing client data to ungoverned AI systems.

Phase 5 - Scale, Iterate, and Optimize

Multi-year waterfall programs are how transformation initiatives die slowly. Sprint-based delivery (90-day cycles with defined outcomes) lets institutions deliver value incrementally, gather real feedback, and adjust before investing further.

Change management is where most programs actually fail. Research consistently shows that digital transformation failure rates hover around 70%, with adoption gaps and lack of executive sponsorship as primary causes. Technology that staff don't trust or understand simply doesn't get used. The ROI never materializes, regardless of how well the system was built.

Executive sponsorship, structured training, and visible quick wins in the first 90 days are as important as the technical architecture.

Governance, Security, and Regulatory Compliance: The Non-Negotiable Foundation

Institutions that retrofit compliance controls after deployment face remediation costs that dwarf the original implementation savings. Starting without a compliance-first architecture isn't a shortcut - it's a deferred penalty.

Regulatory frameworks including SEC Rule 17a-4, FINRA 3110, GDPR, SOX, and GLBA mandate auditability, data retention policies, access controls, and breach notification procedures. Each of these has enforcement teeth. Build for them from day one.

Cybersecurity and Zero Trust Architecture

Financial institutions face a concentrated attack surface. Phishing, ransomware, API vulnerabilities, and third-party risk have all intensified - and the consequences are measurable. The IBM Cost of a Data Breach Report 2024 found the financial industry consistently faces the highest breach costs of any sector.

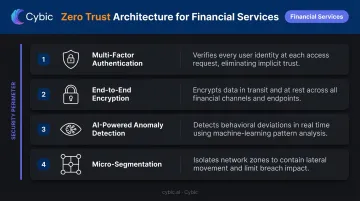

Zero Trust is the architectural response to this environment. Rather than assuming internal network traffic is safe, every user, device, and access request is verified regardless of origin. Key implementation measures:

- Multi-factor authentication across all access points

- End-to-end encryption in transit and at rest

- AI-powered anomaly detection for real-time threat identification

- Micro-segmentation to contain lateral movement after a breach

AI Governance and Responsible AI

As AI makes credit decisions, flags suspicious transactions, and generates customer recommendations, governance frameworks must address:

- Whether model outputs are systematically disadvantaging any customer segment (bias monitoring)

- Whether a compliance officer can explain why a credit application was declined (explainability)

- Which decisions require human review before action (escalation policy)

- Whether every AI-driven decision is logged with enough context for regulatory review (audit trails)

Cybic embeds these governance requirements - RBAC, auditability, AI lifecycle management, and strict data governance including no model training on proprietary enterprise data - directly into system architecture. The result is that compliance controls don't follow deployment; they ship with it.

Data Governance Essentials

A functional data governance program covers:

- Data classification by sensitivity level (PII, financial data, internal-only)

- Access permissions aligned to compliance roles via RBAC

- Automated data retention and lifecycle management

- Complete audit trails for AI-driven decisions

Data governance is also the prerequisite for scaling AI. Models trained on poorly governed data produce unreliable outputs - and in a regulated environment, that means compliance exposure, not just a performance problem.

How to Measure Success: Metrics and ROI for Financial Services DX

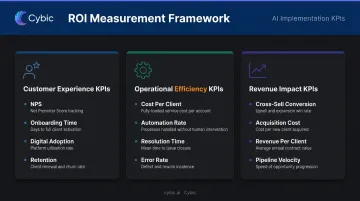

Vanity metrics - number of apps launched, digital login counts - don't belong in board reporting. The KPIs that matter fall into three categories:

Customer Experience

- Net Promoter Score (NPS) trend over rolling quarters

- Client onboarding time (days from application to account open)

- Digital channel adoption rate

- Client retention rate by segment

Operational Efficiency

- Cost per client served

- Process automation rate across targeted workflows

- Time to resolution for service requests

- Error rate comparison: automated vs. manual workflows

Revenue Impact

- Cross-sell and upsell conversion rates

- New client acquisition cost

- Revenue per client

- Pipeline velocity (time from lead to close)

McKinsey's research on banking productivity shows that institutions with mature digital programs achieve meaningful productivity gains through workflow simplification and automation - but realizing those gains requires measurement infrastructure to be in place before implementation begins.

Baseline measurements established before deployment make ROI attributable. Without them, improvements are real but not reportable, which means they don't influence board strategy or future investment decisions.

Continuous measurement - not a one-time post-project review - is what distinguishes institutions that compound their transformation gains from those that declare victory and stagnate.

Frequently Asked Questions

What is digital transformation in financial services?

It's the strategic integration of technology to reimagine customer experiences, improve operations, and evolve business models while navigating the regulatory and security requirements specific to the financial sector.

What are the biggest challenges of digital transformation in financial services?

Legacy system complexity, regulatory compliance demands, and internal skills gaps in AI and data engineering are the most common blockers. Programs that fail typically underestimate how much two or three of these compound each other.

How long does digital transformation take for a financial services firm?

Foundational capabilities (CRM deployment, automation of specific workflows) can go live in three to six months. Full enterprise transformation typically runs 12 to 24 months or longer. Sprint-based delivery is the best way to generate value before the full program completes.

What role does AI play in financial services digital transformation?

AI accelerates transformation across fraud detection, personalization, compliance monitoring, document processing, and advisor productivity. Before scaling into regulated workflows, firms need governance in place: audit trails, explainability, and access controls.

How do financial institutions maintain regulatory compliance during digital transformation?

Embed governance controls into the architecture from day one: data classification, RBAC, audit trails, and AI explainability. Retrofitting these after deployment is significantly more costly and introduces compliance risk.

How do you measure the ROI of digital transformation in financial services?

Track metrics across three categories: customer experience outcomes, operational efficiency gains, and revenue impact. Establish pre-implementation baselines so improvements are attributable and credible for executive and board reporting.